Financial Statement Fraud: Understanding and Preventing the Hidden Threat

Financial statement fraud is the intentional misrepresentation or manipulation of a company's financial data to mislead investors, creditors, and regulators, often through revenue recognition fraud and expense manipulation.

Table of Contents

[ show ]- Loading table of contents...

According to the Association of Certified Fraud Examiners' (ACFE) Occupational Fraud 2026: A Report to the Nations, financial statement fraud accounted for just 6% of the 2,402 cases studied, but it caused the highest median loss of any fraud category, at $1 million per case, ten times the median loss from asset misappropriation.

For risk, fraud, compliance, and underwriting teams at banks, credit unions, fintechs, lenders, and other organizations that verify financial documents, that combination, rare but catastrophic, makes early detection a priority. This guide explains how financial statement fraud happens, why it is hard to detect, which red flags matter most, and how techniques such as vertical and horizontal analysis, internal controls, ethics programs, legal enforcement, and AI-powered document fraud detection can help prevent losses.

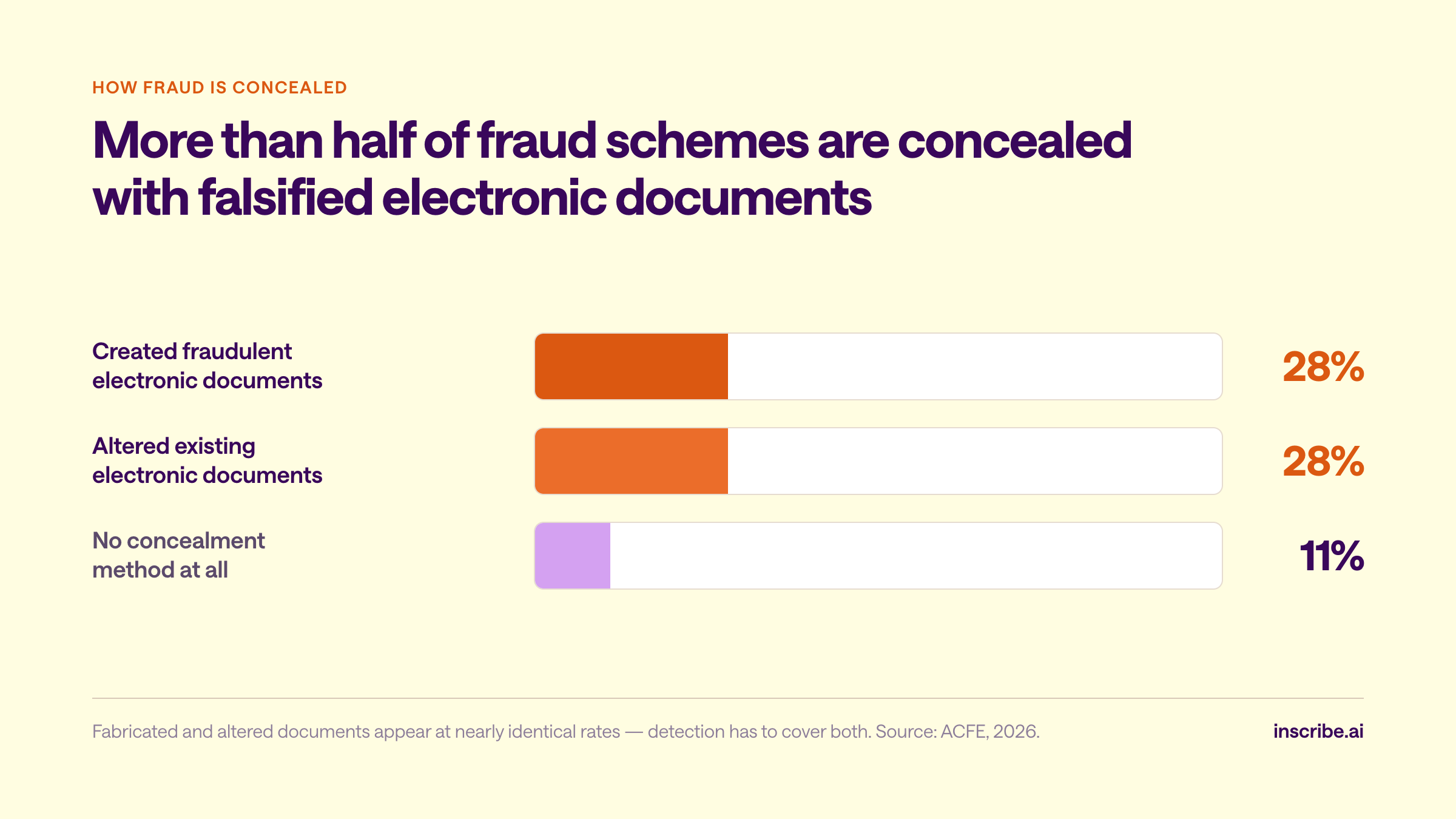

Falsified documents sit underneath most of it. The ACFE found that fraudsters created fraudulent electronic documents in 28% of cases and altered existing electronic documents in another 28%, while only 11% of frauds involved no concealment method at all. Organizations using AI detection have reported preventing millions in fraud losses while reducing document review time by up to 99%, which is why financial statement fraud detection increasingly starts with the source documents, including bank statements, invoices, and tax records, before falsified data reaches financial statements, auditors, or decision-makers.

See how Inscribe detects financial statement fraud

Switch to your desktop to see the interactive product tour!

What is financial statement fraud?

Financial statement fraud is the intentional misrepresentation or manipulation of financial information with the objective of misleading investors, creditors, and regulatory bodies. It undermines the trust stakeholders place in a company's financial statements, and it exposes both the company and individuals involved to civil and criminal liability under fraudulent financial reporting statutes.

According to the Association of Certified Fraud Examiners, this type of fraud typically shows up as:

- Revenue manipulation and improper recognition

- Valuation discrepancies, including improper asset valuation inflating property or inventory values

- Liability concealment and underreporting, where concealed liabilities hide actual debts from financial statements

- Improper disclosures and accounting changes

- Material misstatements affecting operating results

Organizations and individuals commit fraud by placing false or misleading information into a company's financial statements to make the company's financial position look stronger, whether to keep a struggling business afloat, inflate stock value, hit analyst projections, justify executive compensation tied to performance, or qualify for loans and credit lines they would not otherwise secure.

Why is financial statement fraud so hard to detect?

Financial statement fraud is hard to detect because the people committing it are typically the same people responsible for producing and reviewing the financial statements, which means the evidence is deliberately hidden inside the same records auditors rely on. Detecting it takes ratio analysis, historical comparison, and a read on accounting irregularities that distort the picture of a company's financial health, not just a check that the numbers add up.

Seniority makes it worse and it makes it more expensive. The ACFE found that frauds committed by owners and executives carried a median loss of $475,000 and ran for 23 months before detection, against $50,000 and eight months for employee-perpetrated frauds. Senior management is often in a position to override the controls meant to catch them, and the longer a scheme runs the more the surrounding records get shaped to support it.

Concealment is where the document layer comes in. In the ACFE's data, fraudsters created fraudulent electronic documents in 28% of cases and altered existing electronic documents in another 28%. Only 11% of frauds involved no concealment method at all. Those two categories, fabricated from scratch and altered from a real original, show up at nearly identical rates, which means detection coverage has to address both.

One of the clearest warning signs in the numbers themselves: revenue growth that is not matched by a corresponding increase in cash flow. A dedicated internal and external audit function, a proactive board, and an anonymous reporting hotline all measurably improve detection rates. Still, the ACFE's 2026 report found that tips remain the single most common way fraud comes to light at 43% of cases, while external audits surface only 4%. The mechanism most stakeholders assume is catching this fraud largely is not. It also found behavioral red flags present in 84% of cases.

What are the financial statement fraud red flags to watch for?

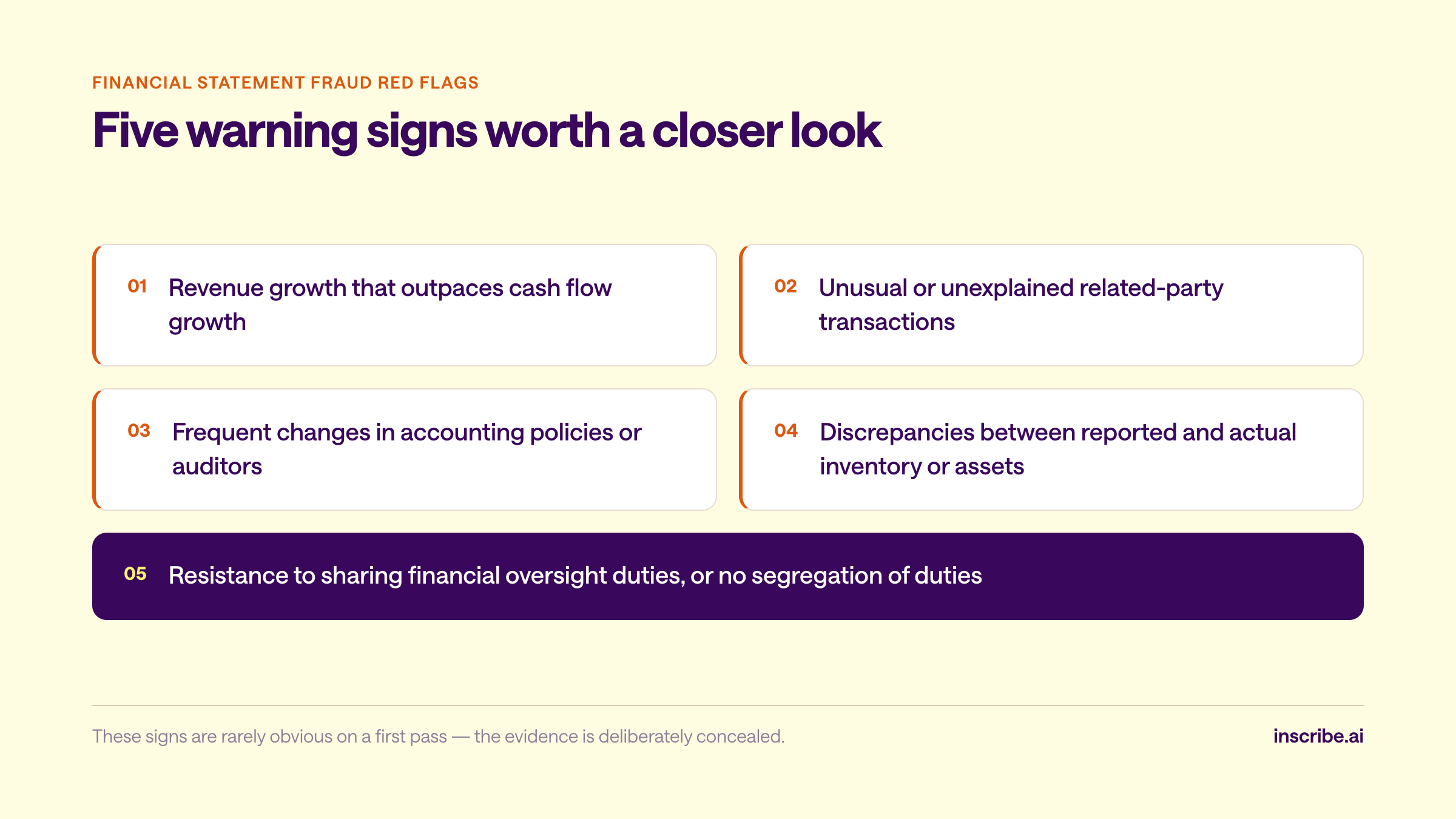

Recognizing red flags is central to detecting and preventing financial statement fraud. Common indicators include:

- Revenue growth that outpaces cash flow growth

- Unusual or unexplained related-party transactions

- Frequent changes in accounting policies or auditors

- Significant, unexplained discrepancies between reported and actual inventory or assets

- Resistance to sharing financial oversight duties, or a lack of segregation of duties

The challenge is that people committing financial statement fraud actively conceal the evidence, so these signs are rarely obvious on a first pass. Comparative ratio analysis is one of the more reliable techniques auditors use, since it surfaces unusual relationships in financial position and performance that warrant a closer look.

Financial statement fraud prevention and detection: analytical techniques

Two techniques form the backbone of financial statement fraud prevention and detection programs.

Vertical analysis assesses each line item on a financial statement as a percentage of total revenue, which helps highlight discrepancies that deserve further investigation.

Horizontal analysis evaluates how financial statements change over time by expressing current figures as a percentage of a base-year amount, making it easier to spot trends and patterns consistent with manipulation. Both are standard in accounting fraud and improper revenue recognition reviews, where the goal is to flag anomalous shifts across periods and ratios.

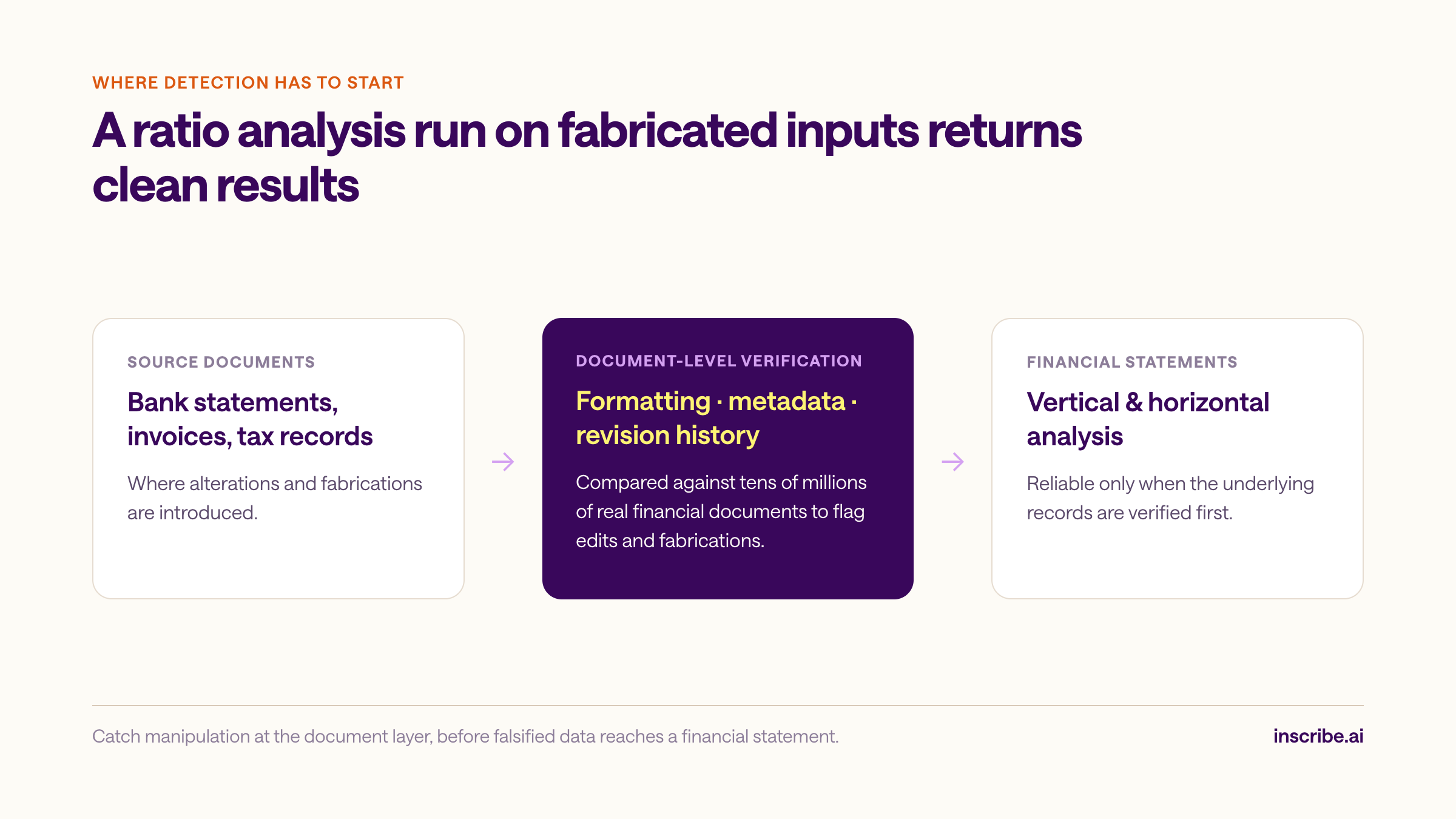

Both techniques are more effective when paired with document-level verification: confirming that the underlying bank statements, invoices, and source records feeding into the financial statements have not themselves been altered or fabricated. A ratio analysis run on fabricated inputs returns clean results. Audit procedures still matter, because technology should support audit evidence and auditor judgment rather than replace them, but a scheme concealed with fake documents will hold up against analytical review until someone checks the documents themselves.

Financial statement fraud examples: real-world cases

- Wells Fargo: From 2002 to 2016, employees opened millions of unauthorized accounts to hit sales targets, forging customer signatures, creating PINs to activate debit cards customers never requested, and altering contact information so customers wouldn't discover the accounts.

- Bernie Madoff: Madoff's Ponzi scheme defrauded roughly 4,800 clients, with nearly $65 billion in fabricated account statement value on the final statements sent to investors in November 2008. Actual principal invested was closer to $17.5 billion. The scheme ran on millions of pages of falsified account statements and trade confirmations documenting transactions that never occurred.

- Enron: Enron used mark-to-market accounting to book projected future profits as current earnings, inflating its reported financial performance, while moving losses and debt off the balance sheet through special purpose entities. The restatement led to one of the largest bankruptcies in U.S. history.

- Colonial Bank: Following a massive mortgage fraud operation involving Taylor, Bean & Whitaker, Colonial collapsed in 2009. The Department of Justice detailed how Lee Farkas and others diverted nearly $3 billion by selling nonexistent mortgage assets and multi-selling legitimate loans. Farkas received a 30-year prison sentence for the scheme, which cost the FDIC approximately $2.96 billion. Legal settlements later recovered nearly $400 million from auditors who missed the deception.

The through line is documentation. In each case the numbers on the statements were supported by records that were forged, fabricated, or describing assets that did not exist, and those records passed through auditors, counterparties, or lenders who had no practical way to test them. That is the point in the chain where document-level verification changes the outcome.

How to detect and prevent financial statement fraud

Preventing financial statement fraud requires a multi-layered approach.

Strengthen internal controls. Segregating accounting duties so no single person controls an entire transaction is one of the most effective structural deterrents. Regular reconciliations between subledgers and the general ledger surface discrepancies while they are still small enough to explain. Independent audits reinforce both, verifying that controls are functioning as designed, and the audit committee should own oversight of that process. Scale matters here: the ACFE found that small organizations were far less likely than large ones to have all 18 anti-fraud controls it studied in place, which is less about small companies attracting more fraud than about having fewer mechanisms available to catch it.

Build a culture of ethics. Ethical leadership sets the standard the rest of the organization follows. Fair employment practices, an open-door policy, and clear written policies all contribute to a culture where fraud is less likely to take root. Pressure from senior personnel is a recurring factor in how these schemes start, which is why tone at the top shows up in enforcement records as often as it does.

Adopt anti-fraud technology. The ACFE's 2026 report found that schemes detected within six months had a median loss of just $40,000, and about a third of frauds were caught that quickly, while longer-running schemes caused dramatically more damage. That makes early detection one of the highest-leverage investments available. Inscribe's automated document fraud detection software checks the source documents rather than the summary figures, comparing formatting, metadata, and revision history against tens of millions of real financial documents to flag alterations and fabrications before manipulated numbers reach a financial statement.

“Inscribe was the inflection point for us. It transformed fraud detection from a manual, subjective process into a scalable, transparent system we can trust every time.” Michael Coomer, Director of Fraud Management at BHG Financial, has described how Inscribe changed what his team treats as a good customer, since a clean-looking application built on manipulated documents is a different risk than it appears to be.

What are the risk factors for financial statement fraud?

Internal risk factors include weak internal controls, insufficient authorization processes, poor segregation of duties, and inadequately disclosed related-party transactions. External risk factors include competitive pressure, economic downturns, and a management team fixated on short-term targets. In practice, financial statement fraud occurs when sustained pressure to meet targets overrides financial integrity, and any combination of these factors raises the likelihood that it will go undetected.

What happens if you falsify financial statements?

Falsifying financial statements is a federal offense in the U.S. Public companies are required to maintain internal controls over financial reporting under the Sarbanes-Oxley Act, enacted in 2002 to prevent fraud and strengthen investor confidence. The Securities and Exchange Commission has authority to impose civil penalties, and individuals can face criminal prosecution and imprisonment for falsification, including misleading disclosures involving related parties. Beyond legal exposure, falsified statements cause lasting reputational damage and erode the trust of investors, lenders, and customers, often permanently.

Financial reporting frameworks like GAAP and IFRS exist precisely to hold organizations to a consistent, verifiable standard, and staying compliant with them is a baseline defense against both accidental misstatement and intentional fraud.

Safeguard against financial statement fraud with Inscribe

Combating financial statement fraud takes vigilance, strong internal controls, and technology that can catch manipulation at the document level before it ever reaches a financial statement. Inscribe's AI agent automates that first line of defense, screening the bank statements, tax forms, and financial records that feed into underwriting and risk decisions, freeing up fraud and risk teams to focus on higher-level investigation instead of manual document review.

For the wider picture of how falsified paperwork moves through financial services, see our guide to document fraud and the 2026 State of Document Fraud Report. If bank statements are your highest-volume document type, start with Inscribe's fake bank statement detector.

Talk to one of our experts to see how Inscribe can help your organization detect and prevent financial statement fraud.

Financial statement fraud FAQs

Financial statement fraud involves the deliberate misrepresentation or manipulation of financial information to deceive stakeholders. This unethical practice can significantly distort a company's financial health and performance.

Financial statement fraud occurs when financial information is intentionally misrepresented or manipulated to deceive stakeholders and create a false perception of a company's financial condition. This can involve inflating revenues, understating expenses, manipulating reserves, overvaluing assets, using improper accounting methods, and participating in fraudulent transactions. Perpetrators may also attempt to conceal their actions by creating falsified documentation and colluding with external parties, all with the objective of misleading investors, creditors, and regulatory bodies.

The most common type of financial statement fraud is revenue recognition fraud. It involves manipulating revenue figures in the financial statements to create a false impression of higher sales or better financial performance. Perpetrators may engage in practices like recording fictitious sales or prematurely recognizing revenue. Revenue recognition fraud is enticing because it can significantly impact reported profitability and influence investor decisions, potentially boosting stock prices.

Companies manipulate financial statements through various methods, including recording fictitious revenues, understating expenses, overvaluing assets, using improper accounting practices, engaging in fraudulent transactions, and falsifying documentation. These unethical practices distort financial figures like revenue, expenses, assets, and liabilities, leading to severe legal and financial consequences, such as penalties and loss of stakeholder trust.

Yes, financial statement fraud is typically considered a crime. Financial statement fraud involves intentionally misrepresenting a company's financial information in its financial statements, such as the balance sheet, income statement, and cash flow statement. This can involve inflating assets, understating liabilities, manipulating revenue figures, or engaging in other deceptive practices to make the company appear financially healthier than it actually is. Engaging in financial statement fraud can have serious legal consequences, including both civil and criminal penalties.

Financial statement fraud involves intentionally misrepresenting a company's financial information in its financial statements to deceive investors, creditors, or other stakeholders. Some examples include manipulating the timing of revenue recognition, creating fictitious sales, and engaging in other deceptive practices to present a false picture of their financial performance. This type of fraud can lead to legal consequences, loss of investor trust, and financial instability for the company when discovered. It also harms investors who rely on accurate financial statements to make informed decisions.

Falsifying financial statements is a serious offense that can have significant legal, financial, and reputational consequences for individuals and organizations.It's important to note that the specific consequences can vary depending on the jurisdiction, the nature and scale of the fraud, and the applicable laws and regulations. Companies and individuals should prioritize ethical and transparent financial reporting to avoid the severe legal and financial repercussions associated with falsifying financial statements.

Yes, manipulating financial statements is illegal. It constitutes fraudulent activity and can lead to serious legal consequences. Financial statements are a critical component of a company's financial reporting and are used by investors, creditors, regulators, and the public to assess the financial health and performance of an organization. Deliberately manipulating financial statements undermines trust, misrepresents a company's financial position, and can harm investors and stakeholders.

About the author

Ronan Burke is the co-founder and CEO of Inscribe, where he has spent nearly a decade studying how fraud evolves and what it takes to stop it. His work sits at the intersection of generative AI and financial crime: specifically, how AI-powered reasoning can outpace the fraud tactics that have already outrun rules-based detection. He writes and speaks regularly on document fraud, agentic AI, and what it means to build fraud defenses for a world where fakes are cheap, fast, and convincing.

Learn More

Dive deeper into document fraud

What will our AI Agents find in your documents?

Start your free trial to catch more fraud, faster.