See beyond the document by enriching every applicant with public data

Table of Contents

[ show ]- Loading table of contents...

A convincing document doesn't always tell the truth. A bank statement may appear authentic. A pay stub may look legitimate. A business registration may contain valid information. But documents only tell part of the story. The real question isn't simply whether a document looks real, it's whether the story the applicant is telling holds up.

That's why Inscribe expands every investigation beyond the document itself. Our agentic AI analyzes what happens inside the document, compares findings across related documents, and validates claims against trusted public and third-party data. Instead of relying on a single piece of evidence, risk teams receive a complete picture of the applicant before making a decision.

The result is a more accurate understanding of customer risk.

Customer-level analysis starts where document analysis ends

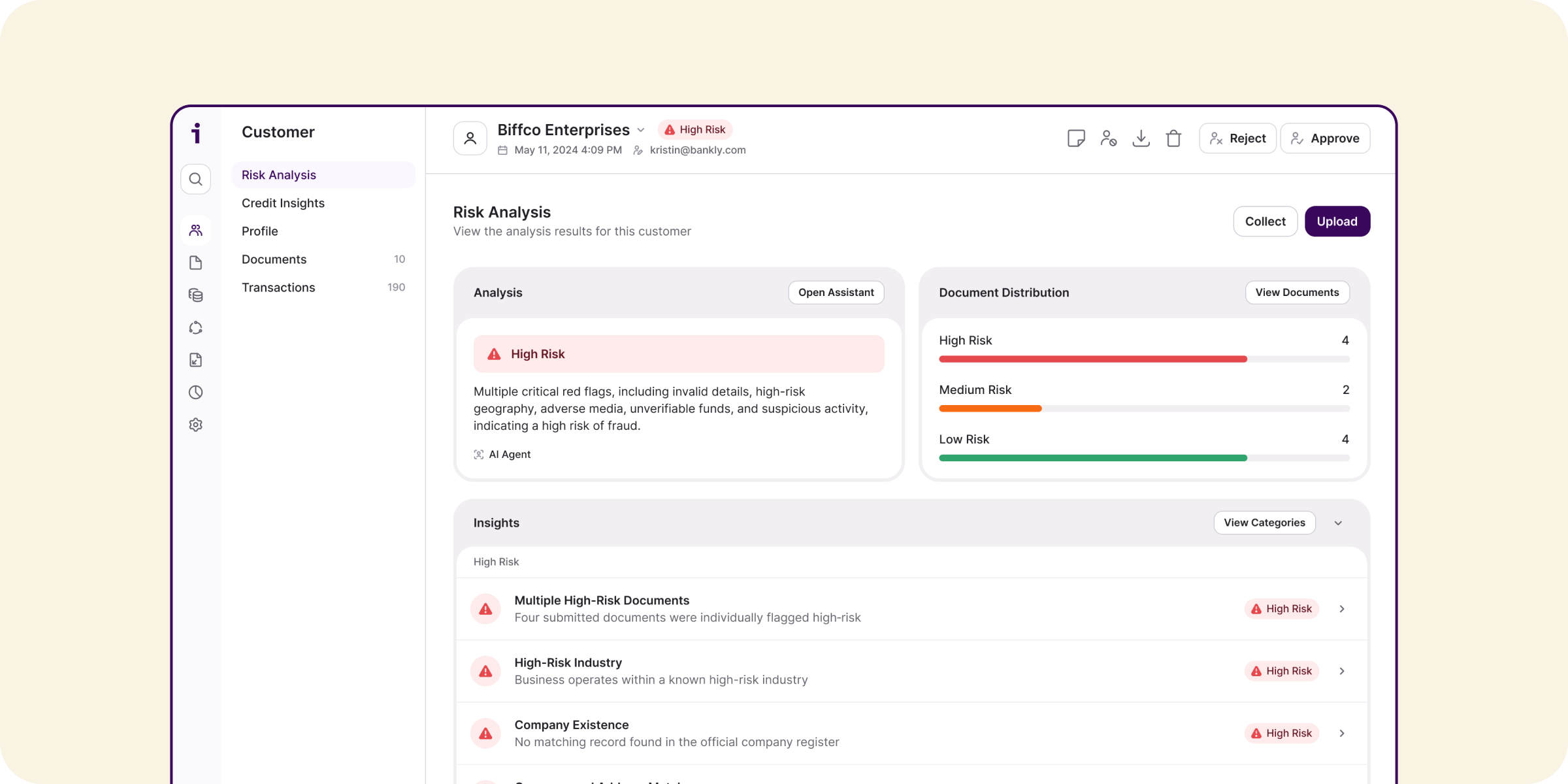

Every submitted document receives its own fraud assessment, surfacing evidence of manipulation, AI-generated content, forensic anomalies, and other suspicious behavior. But financial institutions don't make decisions on individual documents, they make decisions on customers.

That's why Inscribe rolls findings across every submitted document into a unified customer risk profile. Document fraud signals, cross-document insights, and public data verification come together in a single customer risk assessment, giving analysts one place to understand overall customer risk and the factors driving it.

Fraud rarely happens in isolation. An altered bank statement may seem suspicious on its own, but when combined with inconsistencies across other submitted documents, repeat applications, or conflicting income information, a much clearer picture begins to emerge.

Inscribe automatically analyzes relationships across every document submitted by an applicant, identifying patterns that would be difficult or impossible to detect through manual review alone. Instead of reviewing documents independently, analysts gain a connected view of the entire application, allowing them to identify coordinated fraud with greater confidence.

Customer-level analysis includes insights such as:

High-risk documents

Identify applicants who submit multiple high-risk documents, indicating broader fraud activity rather than isolated document issues.

High-severity fraud signals

Surface customers with serious fraud indicators appearing across several submitted documents, helping teams prioritize investigations.

Previous fraudulent applications

Identify customers whose documents or identities are linked to previously confirmed fraudulent applications, revealing repeat behavior and organized fraud.

Salary cross-checks

Compare salary information extracted from pay stubs against deposits appearing in bank statements to verify pay periods, payment frequency, bonuses, and income consistency.

Instead of reviewing every document independently, analysts see how evidence connects across the entire application.

Verify document claims with trusted public data

Connecting evidence across multiple documents provides valuable context, but it's still only part of the picture. The next step is validating whether the information an applicant provides matches reality.

To do that, Inscribe enriches every investigation with trusted public and third-party data. Applicant, business, ownership, and address information are automatically validated against authoritative sources, helping teams confirm that the details contained in submitted documents reflect the real world.

These customer-level insights help answer questions that documents alone cannot. Does the business actually exist? Is the applicant connected to the address they provided? Is the listed owner associated with the company? Has the business appeared in adverse media? Is it operating in a high-risk industry or geography?

Customer-level verification includes:

Address verification

Confirm that submitted addresses exist and identify fabricated or suspicious locations.

Person and employer relationships

Verify that applicants are connected to their claimed address and employment.

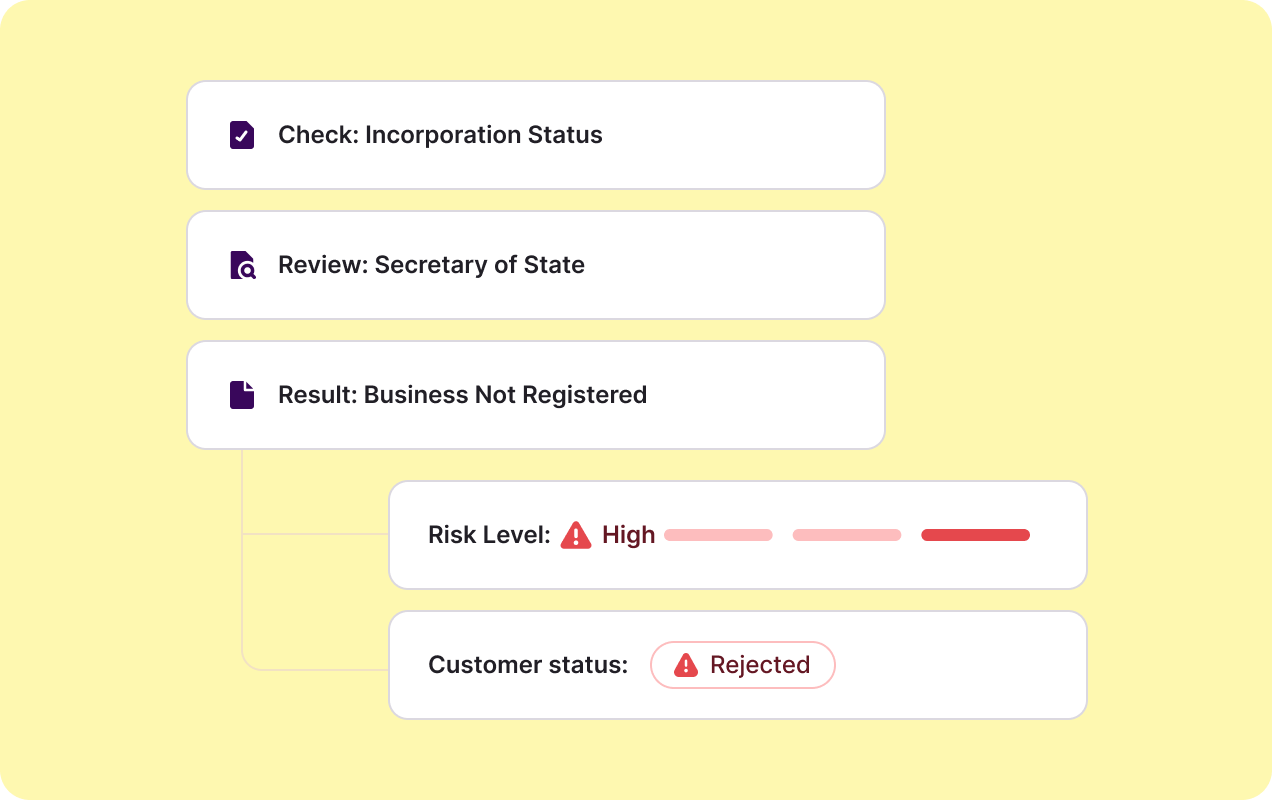

Business verification

Confirm that businesses exist, are active, and are properly registered using Secretary of State records, corporate filings, and other trusted sources.

Ownership verification

Validate that listed owners or principals are genuinely associated with the business.

Web presence

Confirm that businesses have a credible online footprint through websites, directories, or other trusted listings.

Adverse media screening

Surface negative media coverage involving businesses or beneficial owners that may indicate elevated fraud, compliance, or reputational risk.

High-risk geography and industry

Identify applicants operating in higher-risk industries or jurisdictions that warrant additional review.

A complete picture of customer risk

No two organizations evaluate risk the same way. A lender may prioritize income verification, while a bank opening new accounts may care more about business legitimacy, ownership, or adverse media. Compliance teams often weigh geographic and industry risk differently than underwriting teams.

That's why customer-level analysis is fully configurable. Organizations can choose which insights contribute to their overall risk assessment, adjust how heavily different signals are weighted, and tailor Inscribe's customer risk model to reflect their own fraud policies and business objectives.

The result is a customer risk assessment that reflects how your organization evaluates risk, not a one-size-fits-all score.

See how Inscribe’s agentic AI uncovers truth inside and outside the document by starting your free Inscribe trial.

About the author

Stephanie Spangler is the Head of Product Marketing at Inscribe, where she covers AI-powered fraud detection, document risk, and how financial institutions are adopting agentic AI. She writes on the intersection of product and practice — translating what fraud detection technology does into what it means for the risk teams using it.

What will our AI Agents find in your documents?

Start your free trial to catch more fraud, faster.