How to choose bank statement verification software: A buyer's guide

Table of Contents

[ show ]- Loading table of contents...

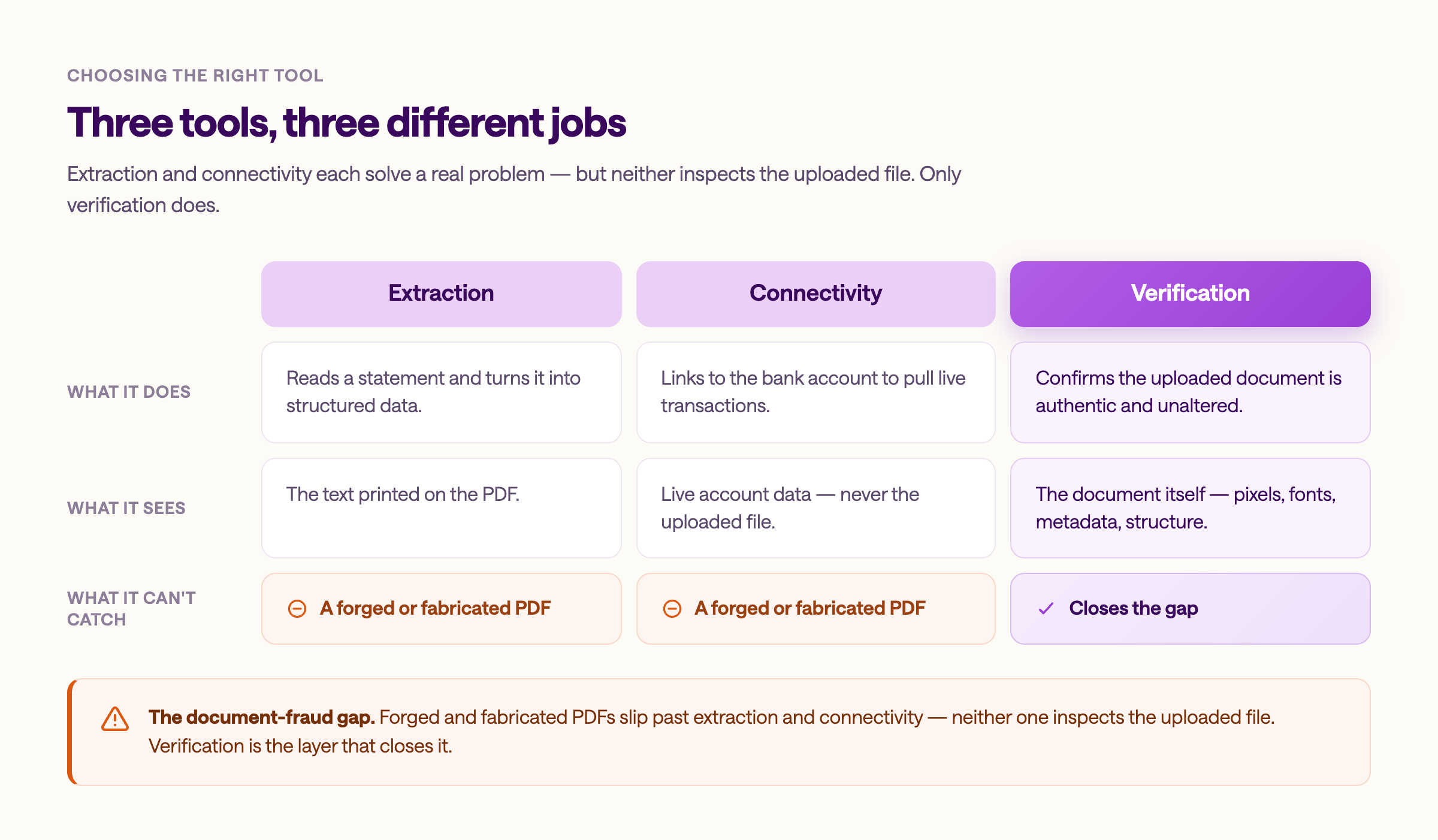

Search for bank statement verification software and you'll find three kinds of tool, each built for a different job. Some are extraction tools that use optical character recognition to read a PDF and pull out balances and transaction history. Some are bank data connectivity feeds, often called open banking, that link to an applicant's bank account and retrieve live transaction data. And some verify whether the document in front of you is authentic and unaltered. Financial institutions often need more than one, so choosing well starts with knowing which job you need done, because the categories are easy to confuse and a mismatch leaves a gap in your pipeline.

When applicants upload PDF statements, the document itself is where forged balances, edited deposits, altered statements, and AI-fabricated files enter your pipeline, so authenticity verification (not just extraction or connectivity) is the capability your risk teams should evaluate most carefully. This guide explains how to choose bank statement verification software for your workflow: the key benefits to weigh, the criteria for assessing any tool, and the questions to ask each vendor before you commit.

Get clear on the job: verification, bank statement extraction, or connectivity

Before comparing vendors, separate the three capabilities that often get marketed together:

- Bank statement extraction reads a statement and turns it into structured data.

- Connectivity, or open banking, links to an applicant's bank account to confirm account ownership and pull live transactions.

- Verification confirms that an uploaded document is real.

Many lenders use more than one. Ask each vendor to state plainly which of the three they provide, and where the other two live in your stack. The distinction matters most with connectivity: a tool like Plaid retrieves live account data once an applicant links their bank, but it never sees the uploaded PDF a borrower submits, so relying on connectivity alone leaves a fraud coverage gap exactly where forged and fabricated statements get in. If a tool's main pitch is data accuracy or cash flow analysis, it is likely built for extraction or connectivity rather than fraud detection.

Detection depth: spotting edits, templates, and fake bank statements

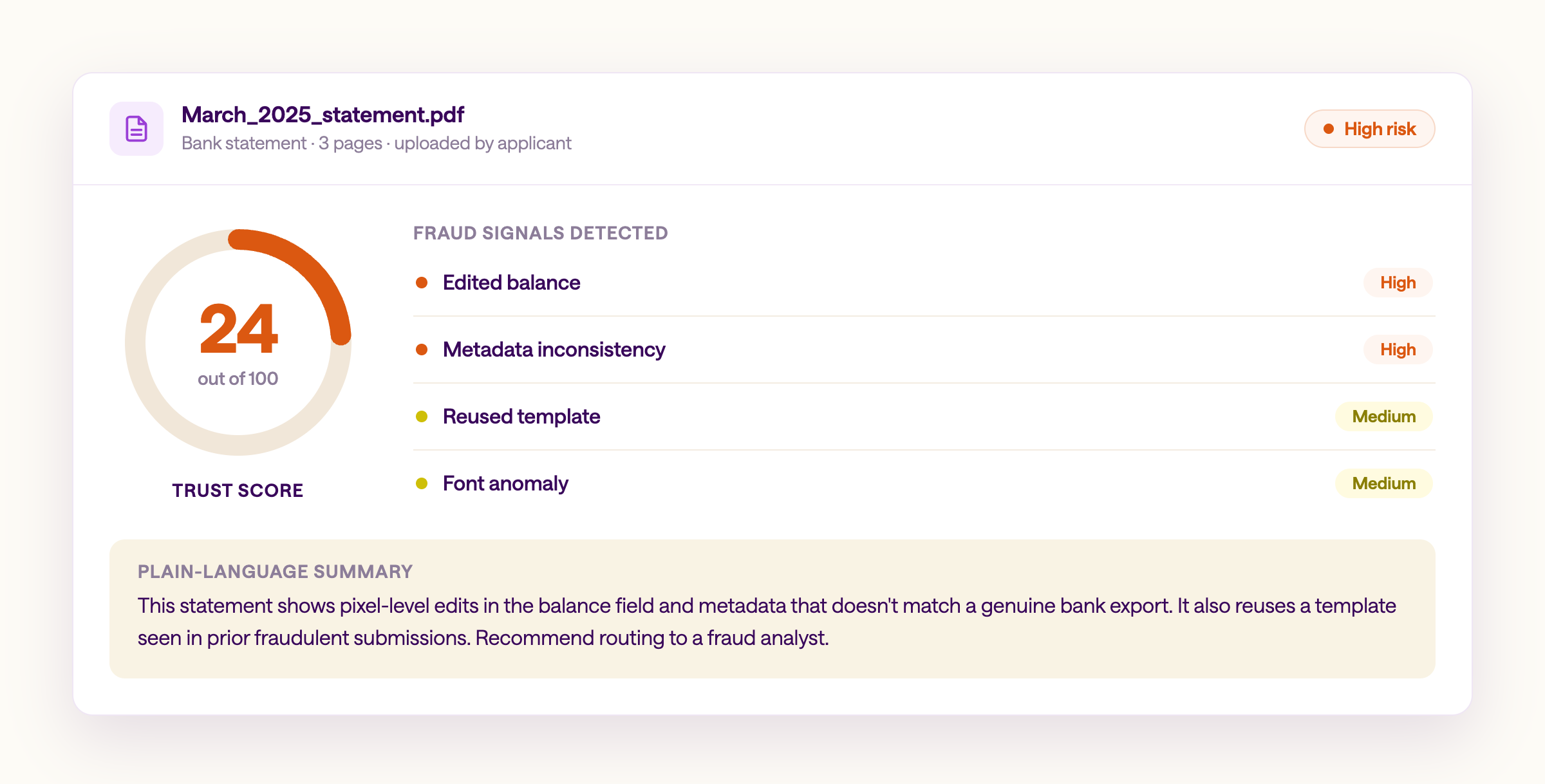

Document fraud has moved well past manual PDF edits. Template generators and multimodal AI now produce fully synthetic statements that look correct to the human eye, and the volume of AI-generated and template-based document fraud has risen sharply. A tool that only flags obvious alterations will miss the fastest-growing category. Look for several layers of document analysis working together, typically driven by machine learning: forensic analysis of metadata, fonts, and file structure; network comparison against patterns seen across many documents; perceptual analysis at the pixel level; and semantic checks for internal contradictions. Together these layers detect fraud that a single check would miss. Ask each vendor whether its detection is tested against current fraud tactics and how often it is updated. Because fully fabricated fake statements are the hardest to catch, see how a tool handles fake bank statements before you rely on it.

Document coverage: match the tool to your document mix

A verification tool is only useful on the documents you actually receive. The key is whether it can verify bank statements that arrive as scanned files, phone photos, and multi-page statements from multiple banks in one pass, beyond the clean digital PDFs from large financial institutions. If your applicants often submit statements from regional banks or credit unions, test how the tool performs outside the major formats, since coverage gaps quietly route files back to manual review, which is the cost you were trying to remove. Coverage also matters for the financial documents that sit alongside statements in income verification, so confirming the full document processing range up front is part of choosing the right bank statement verification software for your book of business.

Evidence over alerts

A flag with no explanation creates work. Your reviewers have to re-investigate to learn why a document scored the way it did, and your auditors need a record they can defend. The better tools return supporting evidence: a clear score, the specific signals behind it, and a plain-language summary an underwriter can read in seconds. Strong tools also validate financial data as they go, surfacing missing data and figures that don't reconcile so the bank statement data you decide on is sound. This matters most in regulated workflows, where KYC, KYB, and AML programs require consistent, documented reasoning. A practical test is whether a sample output is something your fraud or credit team could act on without a data scientist in the room.

Automated bank statement verification: speed and routing

Automated bank statement verification earns its place by clearing authentic statements quickly and reserving your team's attention for the files that warrant it. Manual bank statement verification puts a heavy load on reviewers: Inscribe puts manual review at 10-15 minutes per statement, with results that vary by reviewer experience and workload, and the manual data entry that follows invites human error. Ask how fast results return, whether low-risk statements can clear automatically, and whether high-risk or low-confidence files route to a reviewer with the evidence attached. Inscribe, for example, returns a result in about 72 seconds on average, with authentic statements clearing into downstream bank statement extraction and cash flow analysis while suspicious files are held for review, so genuine applicants move through to loan approvals faster. Make sure the routing thresholds are configurable to your risk tolerance rather than fixed.

Integration and implementation effort

Risk teams and credit teams rarely have spare engineering capacity, so implementation effort is a practical selection factor. The features that reduce it are API-first integration, webhook support for real-time events, and structured outputs that flow into your loan origination, decisioning, and accounting software. Before you commit, confirm a typical integration timeline, what documentation exists, and whether you can pilot ahead of a full rollout.

Security, compliance, and proof points

Verification handles sensitive data, so governance belongs in your evaluation from the start. The essentials are certifications such as SOC 2 Type II and ISO 27001, clear data retention and deletion controls, and outputs that support audit trails and help your team ensure compliance with KYC, KYB, and anti-money laundering (AML) programs. Because regulatory compliance depends on consistent records, ask for proof points from teams like yours, and verify every claim directly. As one example, Inscribe has been purpose-built for document risk screening since 2017 and holds both certifications, giving teams a defensible verification layer across customer onboarding and lending.

Where bank statement verification fits for lenders

In a lending workflow, verification sits inside loan origination, between document collection and the credit decision. When a borrower uploads bank statements at application, it clears the authentic ones automatically and routes only the suspicious files to a fraud analyst, so genuine applicants reach loan approvals faster while your team spends its time on real risk. The same flow supports consumer lending, business lending, and equipment financing, where inflated balances and fabricated deposits would otherwise reach your credit model unchecked.

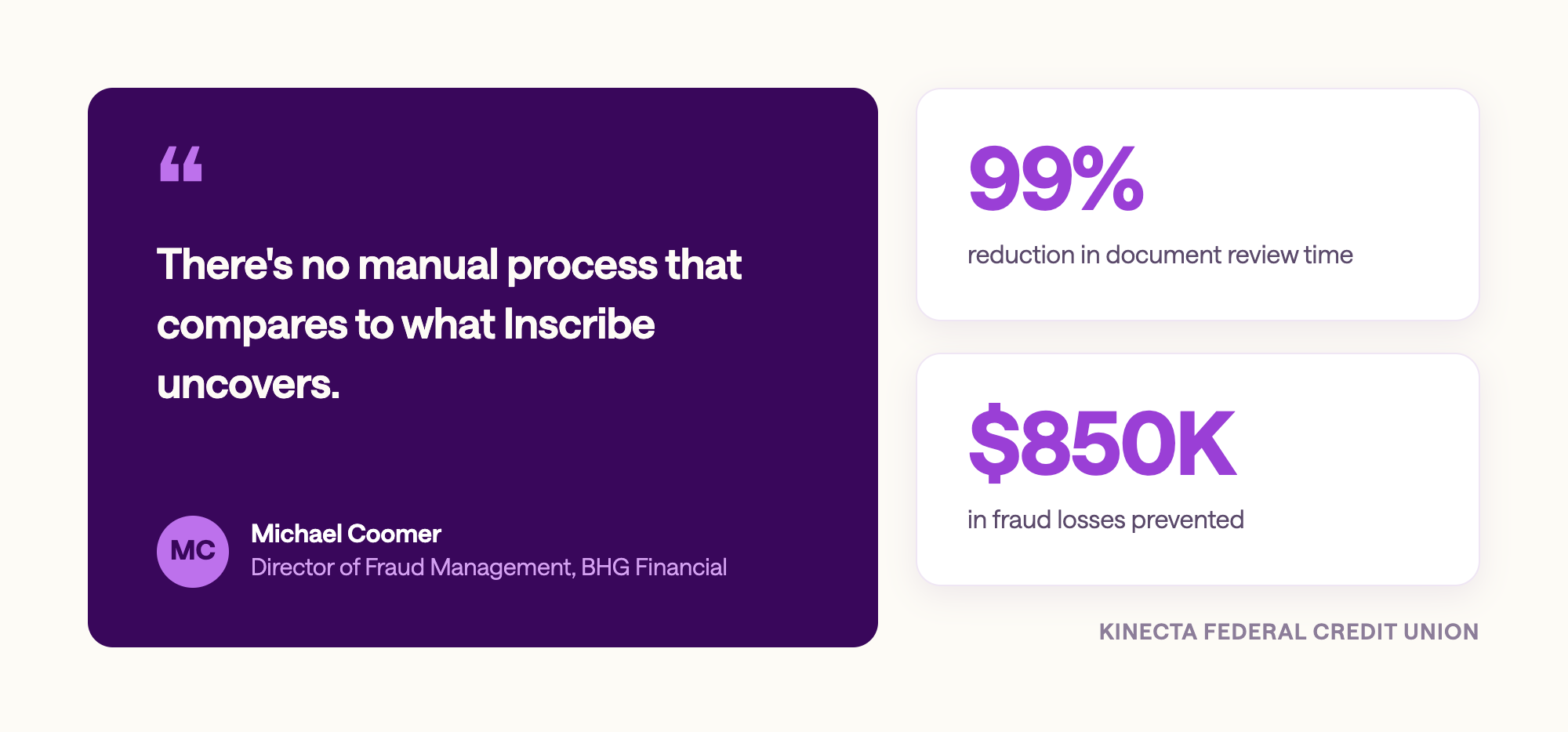

The payoff shows up in lender results. BHG Financial, a non-bank lender, replaced manual fraud detection with a consistent, transparent system for verifying statements at volume. As Michael Coomer, Director of Fraud Management at BHG Financial, puts it: "There's no manual process that compares to what Inscribe uncovers." And at Kinecta Federal Credit Union, where Inscribe runs on documents flagged in the consumer lending workflow, the team cut document review time by 99% and prevented $850,000 in fraud losses.

How to choose bank statement verification software for your workflow

The most reliable way to choose is to map each criterion to your own workflow: the documents and financial records you receive, the fraud risk you are exposed to, the evidence your auditors expect, and the systems your results need to reach. Where your exposure sits in uploaded statements, weight detection depth and explainability above raw extraction speed, since that is where fraud prevention pays off. Where most applicants link live accounts, connectivity may carry more of the load, with verification as the fallback for the files that get uploaded instead. Either way, bank statement verification is one form of document verification, and one step in the broader bank statement analysis process, sitting between document collection and the credit decision in your financial workflows.

Frequently Asked Questions

Prioritize detection depth (whether it catches edited, template-based, and AI-generated statements), coverage for the documents you actually receive, evidence-based explanations rather than bare alerts, configurable routing, fast turnaround, API-first integration, and certifications such as SOC 2 Type II and ISO 27001.

The key benefits are catching forged, edited, and AI-fabricated statements that extraction and connectivity tools miss, faster decisions through automation, consistent and auditable evidence for KYC, KYB, and AML programs, and fewer false positives, so your analysts focus on the files that warrant review.

The bank statement verification process checks whether an uploaded statement is authentic and unaltered. It evaluates the document's integrity (signs of editing), provenance (how and when it was created), and consistency (whether the account holder name, account and routing numbers, and transaction history line up with the rest of the applicant's file and a real bank's format), then returns a score and supporting evidence. Most tools run this verification process automatically, clearing low-risk statements and routing suspicious files to a reviewer.

Data extraction reads a statement and turns it into structured data. Connectivity, or open banking, links to an applicant's account to confirm account ownership and retrieve live transactions. Verification confirms that an uploaded document is authentic and unaltered. They solve different problems, and many lenders use more than one.

Open banking, also called bank data connectivity, links to an applicant's bank account through a feed and retrieves live transaction data. A tool like Plaid is built for this. Bank statement verification software does a different job: it confirms that an uploaded statement is authentic and unaltered. Because a connectivity feed never sees the uploaded PDF, it cannot tell whether a submitted statement is forged or fabricated, so lenders that rely on open banking alone still carry a document fraud gap. Many lenders use both: connectivity for accounts that link, and verification for the statements that get uploaded instead.

Yes, the stronger tools can. Look for layered detection that combines forensic, network, perceptual, and semantic analysis, and confirm the vendor tests against current fraud tactics, since fully synthetic statements are a fast-growing technique.

Manual verification can run 10-15 minutes per statement. Automated verification typically returns a result in around 72 seconds, clearing low-risk statements quickly and routing only high-risk or low-confidence files to a human reviewer.

Common signals include metadata inconsistencies, font and formatting anomalies, pixel-level editing artifacts, recycled templates seen across submissions, altered statements with edited balances, and internal contradictions, such as an account number that does not match the supporting documents.

A score without evidence forces your reviewers to re-investigate and gives auditors little to defend. Tools that surface the specific signals behind a score, plus a plain-language summary, reduce review time and support consistent, documented decisions for KYC, KYB, and AML programs.

It sits between document collection and the credit decision. Authentic statements clear automatically into extraction and downstream analysis without manual intervention, speeding loan approvals, while suspicious files route to a fraud analyst with supporting evidence attached, keeping your reviewers focused on the exceptions that need a closer look.

About the author

Brianna Valleskey is the Head of Marketing at Inscribe, where she has spent nearly five years building the company's go-to-market engine from the ground up. She leads demand generation, SEO and AEO strategy, events, content, and marketing operations — and sits at the center of Inscribe's pipeline strategy, working closely with Sales, CS, and EPD to drive growth. She co-hosts the Good Question podcast and produces Inscribe's annual State of Document Fraud report.

What will our AI Agents find in your documents?

Start your free trial to catch more fraud, faster.