Document fraud statistics: Key facts and trends in 2026

Table of Contents

[ show ]- Loading table of contents...

Document fraud is one of the fastest-growing categories of financial crime, and the data confirms it. Across lending, onboarding, and compliance workflows, fraudulent documents are entering the pipeline at rates that make manual detection unsustainable. The data below draws on the 2026 Document Fraud Report, the LexisNexis True Cost of Fraud Study, the FTC, the Federal Reserve, and Cotality, with each figure attributed to a named source, and primary sources used wherever available.

Inscribe has been purpose-built for document risk screening since 2017 and is trusted by leading banks, credit unions, and fintechs. For a deeper look at how document fraud is evolving and what fraud teams are doing about it, explore the full 2026 Document Fraud Report.

Document Fraud at a Glance

These are the headline numbers from the 2026 Document Fraud Report and the FTC that define document fraud heading into 2026:

- 1 in 16 documents processed across Inscribe's network in 2025 was flagged as fraudulent.

- AI-generated document fraud increased 5x between April and December 2025.

- 97.8% of fraud leaders said they are concerned about AI-enabled document fraud.

- 85.6% of risk leaders said bank statements are the most vulnerable document type.

- $12.5 billion in consumer fraud losses was reported to the FTC in 2024 (FTC Consumer Sentinel Network, March 2025).

How Common Is Document Fraud?

Approximately 6% of all documents processed across Inscribe's network in 2025 were flagged as fraudulent. That translates to roughly 1 in 16 documents showing signs of manipulation, fabrication, or misrepresentation. Inscribe's 2026 Document Fraud Report details how this rate breaks down across document types and industries.

For fraud and risk teams, the math is simple. If your organization processes 10,000 loan applications per year and each application includes three documents, you are potentially looking at over 1,800 fraudulent documents annually. For a team reviewing 500 applications per week, that is roughly 30 flagged documents requiring investigation every week, with volume spiking during holidays and promotional periods.

These rates are consistent with broader industry trends. Approximately 1 in 118 mortgage applications showed indications of fraud in Q3 2025, an increase of 8.2% year over year. For multi-unit properties, the rate was 1 in 26; for investment properties, 1 in 45 (Cotality, 2025 Annual Fraud Report).

Document fraud is not an edge case. It is an operational reality that compounds when detection relies on manual review alone. The Document Fraud Detection Software overview covers how automated detection fits into existing workflows.

Document Fraud Losses and Financial Impact

Every dollar lost to fraud costs North American financial institutions more than $5 in total impact, up 25% since 2021. That multiplier accounts for operational costs, compliance overhead, and reputational damage (LexisNexis True Cost of Fraud Study 2025).

The FTC reported that consumers lost more than $12.5 billion to fraud in 2024, a 25% jump over 2023 (FTC Consumer Sentinel Network, March 2025). While not all of this is document fraud specifically, document manipulation underpins many of these losses, from fabricated income to forged identity documents used in application fraud.

Organizations using AI-powered document verification have reported significant loss prevention:

- BCU prevented $5.6 million in losses from confirmed altered documents in the first nine months of 2025.

- Logix Federal Credit Union prevented over $3 million in potential fraud losses within eight months.

- Kinecta Federal Credit Union saved $850,000 in fraud losses while reducing document review time by 99%.

- Ramp reduced application processing time by 30 minutes per application and saved $300,000 in fraud losses.

For fraud teams, these numbers reframe the ROI conversation. A single detection that prevents a six-figure loss can offset the cost of an entire prevention program.

Most Commonly Forged Document Types

Bank statements are the top concern for fraud and risk leaders. In a survey of 90 fraud and risk professionals published in the 2026 Document Fraud Report, 85.6% cited bank statements as the document type most vulnerable to manipulation. Pay stubs and business financial documents ranked second and third.

Inscribe's detection data shows that fraud pressure is broadly distributed across document types, with most categories exhibiting baseline fraud rates in the 4% to 7% range. Utility bills showed a notably higher flag rate, likely because they are perceived as lower-risk and receive less scrutiny during review. For teams building detection workflows around bank statements specifically, the Bank Statement Analyzer and Fake Bank Statement Detector pages offer detailed context.

Across flagged documents, the data also reveals what fraudsters are changing:

91.2% of flagged documents included altered financial details, either alone or combined with identity changes. The share of documents involving both identity and financial manipulation jumped from 40.2% in 2024 to 59.8% in 2025. These findings come from network-wide detection data published in the 2026 Document Fraud Report.

This dominance of financial manipulation cuts across first-party, third-party, and synthetic identity fraud categories. Detection strategies that focus primarily on identity signals alone will miss a significant share of document-based risk.

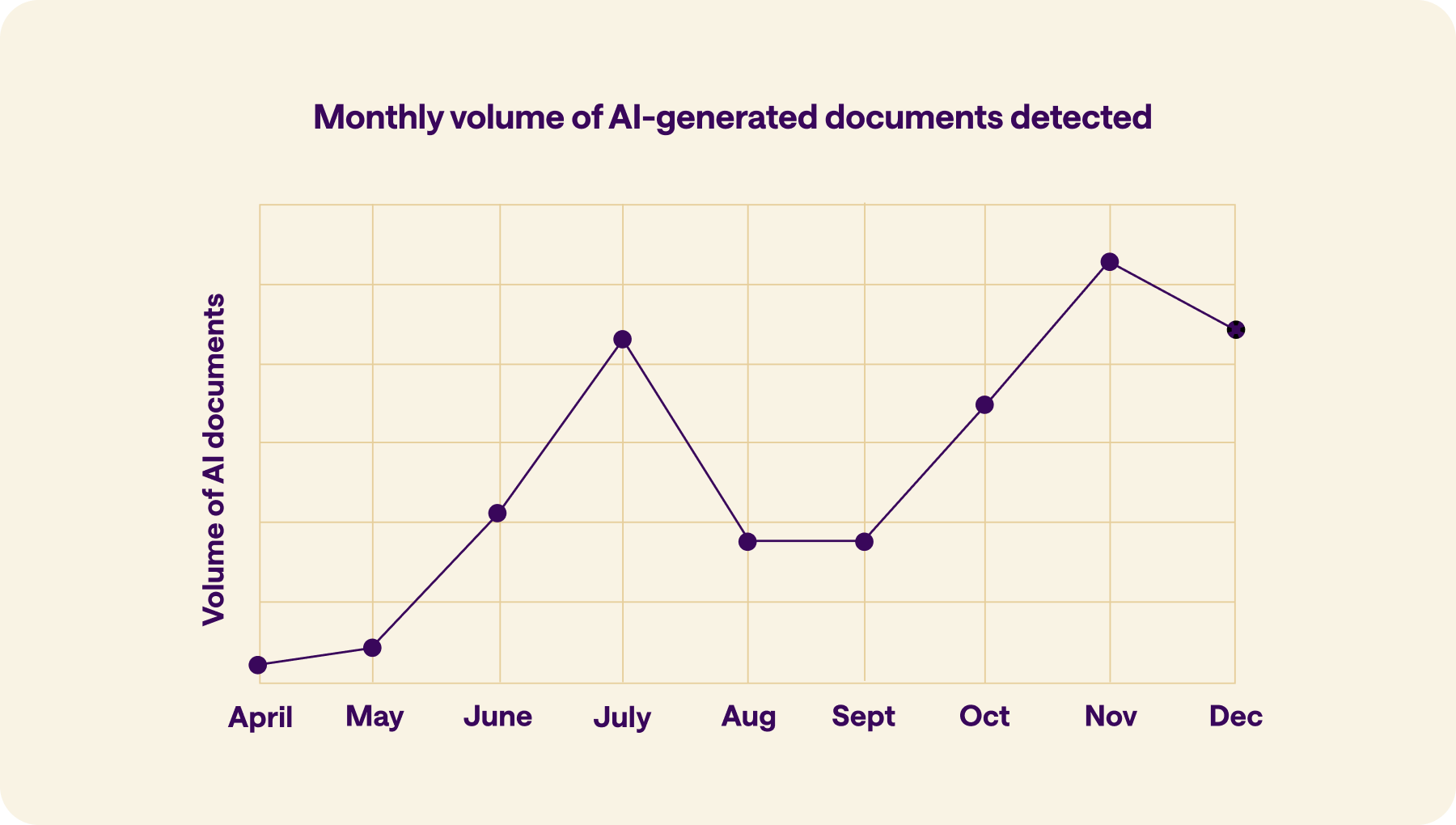

Document Fraud Trends: The Rise of AI-Generated Fakes

Detected AI-generated document fraud increased nearly fivefold between April and December 2025 across Inscribe's network. While AI-generated documents still comprised less than 5% of total fraudulent documents detected, the trajectory is steep and the monthly volume accelerated sharply through late 2025. The 2026 Document Fraud Report tracks this trend in detail.

The concern is reflected in how fraud teams view the threat. In a survey of 90 practitioners, 97.8% expressed concern about AI-enabled document fraud, with 65.6% saying they are "very concerned."

AI-enabled document fraud falls into two patterns. AI-generated documents are created entirely from scratch using image generation models. AI-edited documents start as legitimate files and are modified using generative tools to alter specific fields like names, account numbers, or transaction amounts. Of the two, AI-edited documents currently pose the greater risk because most of the underlying document is genuine, making manipulation harder to catch with surface-level review.

Beyond document creation, AI also serves as a fraud enabler in less visible ways. Practitioners interviewed for the 2026 Document Fraud Report describe how large language models can provide step-by-step document editing guidance, effectively removing the skill barrier that once limited document manipulation. For more on how AI-driven detection addresses these threats, see the AI Fraud Analyst overview.

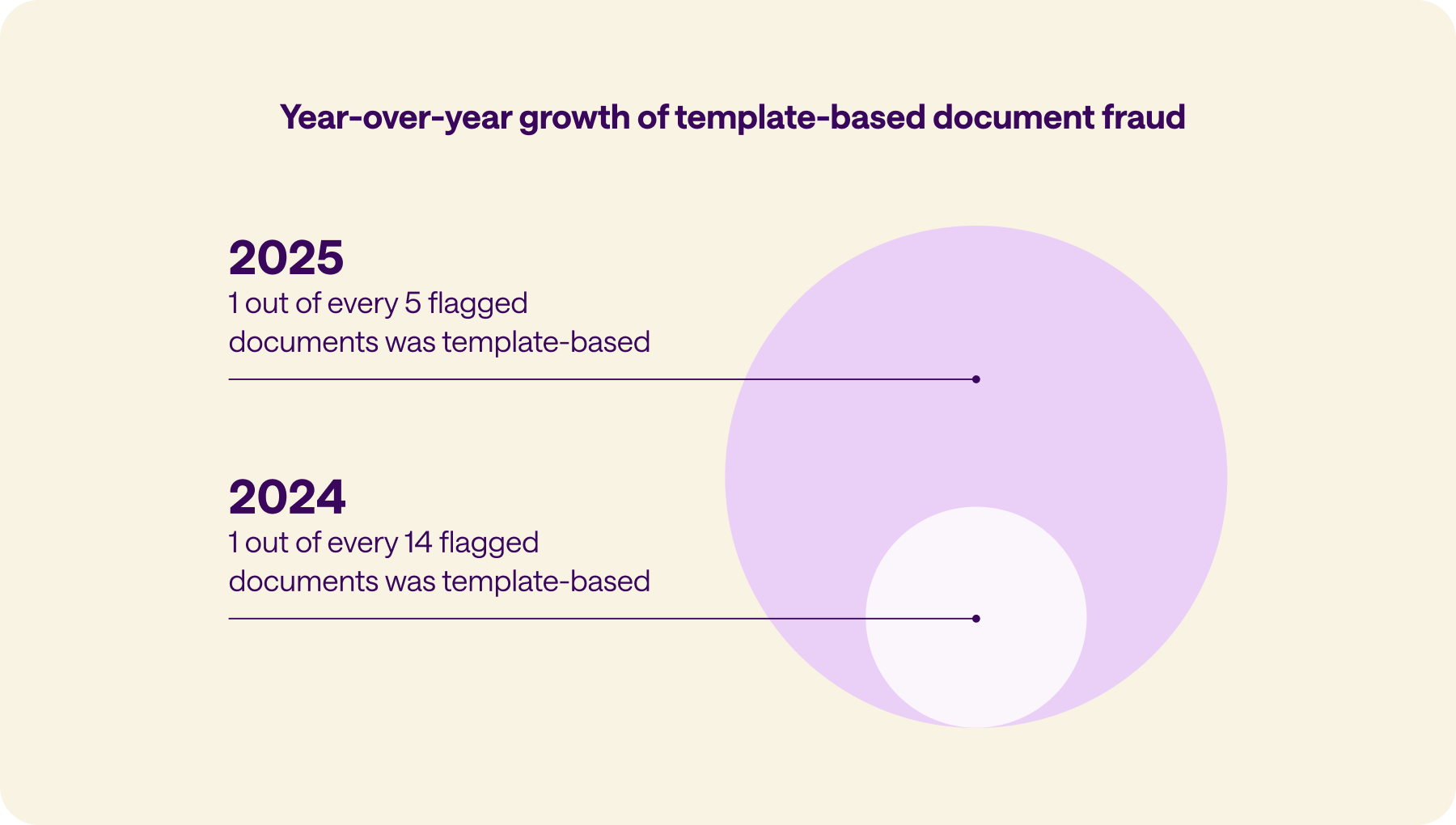

Template-Based Document Fraud Statistics

In 2025, 1 in 5 flagged documents across Inscribe's network showed signs of template-based manipulation, a sharp increase from 1 in 14 in 2024. Despite advances in AI, the most common path for document fraud remains surprisingly low-tech. Online marketplaces sell editable bank statement and pay stub templates for as little as $10, requiring no technical skills to customize and submit. This data is drawn from Inscribe's 2026 Document Fraud Report.

Template-based fraud and AI-generated fraud are not mutually exclusive. Inscribe's detection data shows a growing hybrid pattern: documents that combine purchased templates with AI-assisted editing, making them harder to catch with any single detection method.

Document Fraud by Industry

Document fraud affects any industry where documents are used to establish trust and make financial decisions. The highest-risk sectors include:

Lending (consumer and business): Fraudulent bank statements, pay stubs, and tax forms are used to inflate income and qualify for loans. According to Inscribe's summary of its 2024 Document Fraud Report (prior-year data), over 60% of fraudulent personal loan application documents and 46% of fraudulent SMB loan application documents matched patterns consistent with first-party fraud.

Credit unions and community banks: These institutions face the same fraud pressure as larger banks but often with smaller teams and tighter budgets. Logix Federal Credit Union and BCU are examples of credit unions that have used automated detection to prevent millions in losses. Industry pages for banks, credit unions, and lenders provide additional context.

Mortgage: Fraud risk increased 8.2% year over year in Q3 2025, with approximately 1 in 118 applications showing indications of fraud. Investment and multi-unit properties carry the highest risk: 1 in 45 and 1 in 26, respectively (Cotality, 2025 Annual Fraud Report). Falsified financial information was involved in over 90% of suspected Canadian mortgage fraud cases in H2 2024 (Equifax Canada, H2 2024 Fraud Trends).

Property management and tenant screening: Fake bank statements and proof-of-address documents are submitted during rental applications, particularly in high-volume workflows where manual review varies by reviewer.

Fintech and marketplaces: Onboarding flows for merchants, sellers, and partners are targeted with template-based and fabricated documents during KYB checks and compliance reviews.

Document Fraud Detection Rates

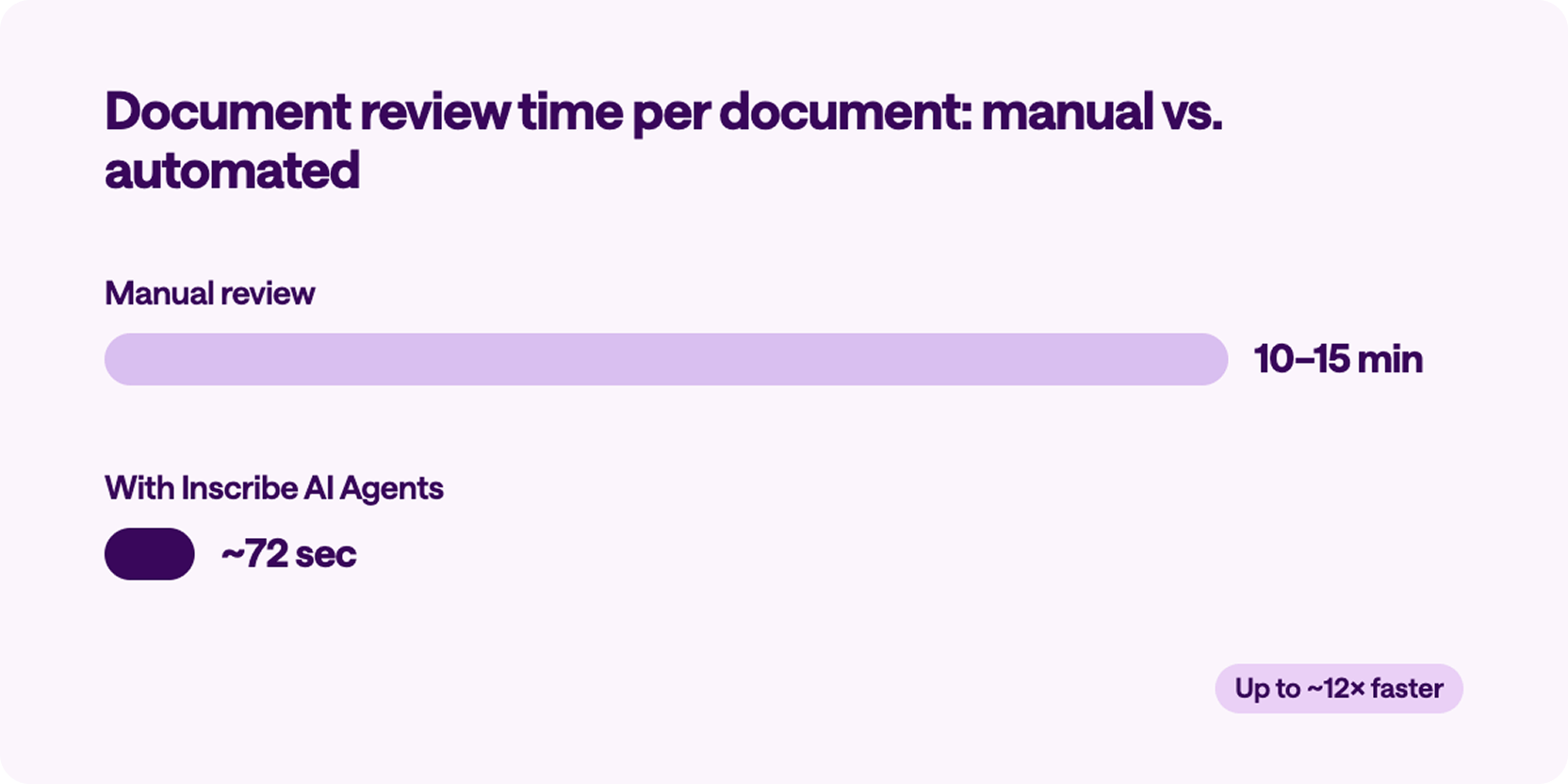

Manual review is resource-intensive and increasingly unreliable. Practitioners interviewed for the 2026 Document Fraud Report described spending 60 to 90 minutes per application on document review before adopting automated tools. At scale, this creates structural bottlenecks that compound as application volume grows.

Automated detection changes the economics. Inscribe's average processing time is approximately 72 seconds per document, compared with the 10 to 15 minutes practitioners reported for manual review. The LexisNexis True Cost of Fraud Study found that 44% of North American financial institutions still rely primarily on manual processes for fraud prevention (LexisNexis, 2025).

For a closer look at how automated document fraud detection fits into verification workflows, the Document Fraud Detection Software page and Demo Center provide detailed walkthroughs.

Document Fraud and Synthetic Identity Fraud

Document fraud and synthetic identity fraud are increasingly intertwined. Synthetic identity fraud involves combining real personal information (such as a legitimate Social Security number) with fabricated details to create a fake identity. The Federal Reserve has identified it as the fastest-growing type of financial crime in the United States (Federal Reserve).

Fraudulent documents are a critical enabler of synthetic identity schemes. Fabricated pay stubs, forged bank statements, and AI-generated identity documents give synthetic identities the supporting evidence they need to pass verification. Losses from synthetic identity fraud crossed the $35 billion mark in 2023, according to anti-fraud platform FiVerity (Federal Reserve Bank of Boston, April 2025).

The growth trajectory is sharp. Sumsub reported a 311% increase in synthetic identity document fraud between Q1 2024 and Q1 2025 (ACFE, 2025). Note: this figure originates from Sumsub's research and is cited here via the ACFE's summary, not a direct primary source.

Inscribe's own network data shows the growing overlap: the share of flagged documents involving both identity and financial manipulation increased from 40.2% in 2024 to 59.8% in 2025, suggesting that fraud categories are blurring. The full breakdown appears in the 2026 Document Fraud Report. Detection strategies that treat identity verification and document verification as separate problems will increasingly miss risk.

Methodology and Sources

Every statistic in this article is attributed to a specific source. Below is the complete list of sources cited, with direct links where available.

Inscribe first-party data

- 2026 Document Fraud Report: Detection data from millions of documents processed across hundreds of financial institutions (January through November 2025); survey responses from 90 fraud and risk leaders (November and December 2025); practitioner interviews with fraud and risk leaders from Discover, BCU, Coast, Rapid Finance, Nymbus, Logix FCU, BHG Financial, Sardine, America's Credit Union, Kinecta, and Point Predictive.

- BCU customer story: $5.6 million in fraud losses prevented.

- Logix Federal Credit Union customer story: Over $3 million in potential fraud losses prevented.

- Kinecta Federal Credit Union customer story: $850,000 saved, 99% reduction in document review time.

- Ramp customer story: $300,000 saved, 30-minute reduction in processing time per application.

Third-party sources

- LexisNexis True Cost of Fraud Study 2025 North America: Fraud multiplier data ($5+ per $1 lost); 44% of FIs rely on manual processes. Survey of 507 risk and fraud executives.

- FTC Consumer Sentinel Network Data Book 2024: $12.5 billion in reported consumer fraud losses in 2024.

- Cotality 2025 Annual Fraud Report: Q3 2025 data; 1 in 118 applications; 8.2% YoY increase; investment and multi-unit segment rates.

- Federal Reserve Synthetic Identity Fraud Initiative: Synthetic identity fraud identified as fastest-growing financial crime in the U.S.

- Federal Reserve Bank of Boston, April 2025: Synthetic identity fraud losses crossed $35 billion in 2023 (citing FiVerity).

- ACFE Top Fraud Trends of 2025: 311% increase in synthetic identity document fraud Q1 2024 to Q1 2025 (citing Sumsub research; secondary source).

- Equifax Canada H2 2024 Fraud Trends (PDF): Over 90% of Canadian mortgage fraud cases involve falsified financial documents.

Get started:

👉 Explore the Demo Center

👉 Start your free trial

👉 Read the full 2026 Document Fraud Report

Frequently Asked Questions

Approximately 6% of all documents processed across Inscribe's network in 2025 were flagged as fraudulent. That is roughly 1 in 16 documents showing signs of manipulation, fabrication, or misrepresentation. For an organization processing 10,000 loan applications per year with three documents each, that translates to over 1,800 potentially fraudulent documents annually. Source: 2026 Document Fraud Report.

Rates vary by loan type and segment. Inscribe's network data shows an overall document fraud rate of approximately 6%. In mortgage lending, about 1 in 118 applications showed indications of fraud in Q3 2025, with rates significantly higher for multi-unit properties (1 in 26) and investment properties (1 in 45) (Cotality, 2025 Annual Fraud Report).

The total cost extends well beyond direct losses. Every dollar lost to fraud costs North American financial institutions more than $5 when accounting for operational costs, compliance, and reputational impact (LexisNexis, 2025).

Bank statements are the top concern among fraud and risk leaders, with 85.6% citing them as the most vulnerable document type. Pay stubs and business financial documents rank second and third. Utility bills show the highest flag rate in detection data, likely because they are perceived as lower-risk and receive less scrutiny during review. Source: 2026 Document Fraud Report.

AI has changed document fraud in two ways. Fraudsters use generative AI to create convincing fake documents from scratch and to edit legitimate documents with precision that can defeat visual inspection. Detected AI-generated document fraud increased nearly 5x between April and December 2025, and 97.8% of fraud leaders express concern about AI-enabled fraud. Source: 2026 Document Fraud Report.

Lending, mortgage, banking, credit unions, tenant screening, fintech, and marketplace onboarding are among the most affected because they rely on documents to verify identity, income, assets, or eligibility.

Yes. AI-based document fraud detection can identify manipulation patterns, metadata anomalies, financial inconsistencies, and cross-document mismatches that are difficult to catch through manual review alone.

About the author

Brianna Valleskey is the Head of Marketing at Inscribe, where she has spent nearly five years building the company's go-to-market engine from the ground up. She leads demand generation, SEO and AEO strategy, events, content, and marketing operations — and sits at the center of Inscribe's pipeline strategy, working closely with Sales, CS, and EPD to drive growth. She co-hosts the Good Question podcast and produces Inscribe's annual State of Document Fraud report.

What will our AI Agents find in your documents?

Start your free trial to catch more fraud, faster.