Document Verification for Lenders: AI-Powered Fraud Detection in Financial Services

Learn how AI-powered document verification helps lenders detect fraud in bank statements, pay stubs, tax forms, and ID documents, faster and more accurately than manual review.

Table of Contents

[ show ]- Loading table of contents...

Introduction

Document verification for lenders validates whether customer-submitted documents are authentic, accurate, and safe to use in underwriting, onboarding, fraud prevention, and regulatory compliance decisions. In lending, the goal is not only to read bank statements, pay stubs, tax documents, business financials, or an identity document; the goal is to verify document authenticity and assess risk before a fraudulent applicant enters the portfolio.

This article focuses on document verification services for fintechs, banks, mortgage brokers, commercial lenders, and other financial institutions that review physical or digital copies during customer onboarding for new customers, account creation, credit underwriting, income verification, address verification, KYB, and high value transactions. It covers the document verification process for bank statements, employment records, tax forms, business documents, utility bills, driver's license, passports, residence permits, and other government issued IDs. It does not cover generic file storage, basic document management, or OCR-only workflows that extract text without fraud analysis.

Document verification for lenders combines automated data extraction with sophisticated fraud detection to validate financial documents and prevent losses from forged, manipulated, synthetic, or AI-generated submissions. Automated document verification leverages advanced technologies, such as artificial intelligence (AI) and machine learning, to fast-track the verification process, analyzing and validating documents with high speed and precision.

You will learn how modern automated document verification solutions:

- Detect fraudulent documents that manual verification processes and legacy tools often miss

- Compare AI-powered verification against manual review and rules-based document validation

- Verify different document categories, including bank statements, pay stubs, tax documents, business financial records, and ID document verification

- Use multiple layers of analysis, including metadata, perceptual signals, network analysis, and external enrichment

- Fit into underwriting, fraud operations, compliance audit preparation, and broader risk management workflows

Effective document verification prevents financial losses, ensures regulatory compliance, and builds trust with users in digital environments. The same principle applies beyond lending: document verification streamlines onboarding in human resources by ensuring that candidates have authentic academic degrees and certifications, and document verification protects buyers, sellers, and agents against fraudulent property deeds in real estate. For lenders, however, document verification important to fraud prevention, security, and onboarding risk because weak controls directly increase credit losses, identity theft, money laundering exposure, customer frustration, and compliance risk.

Understanding Document Verification in Financial Services

In a lending and fraud context, document verification means confirming that submitted documents are genuine, unaltered, internally consistent, and tied to the person or business presenting them. At its simplest, verification is the process of collecting documents, extracting relevant information, validating authenticity, checking the extracted data against trusted databases or other records, and routing edge cases to manual review when necessary.

That definition matters because many document verification solutions stop at optical character recognition. Optical Character Recognition (OCR) technology is commonly used in document verification to extract and validate information from documents, ensuring that the data is accurate and matches the provided information. But optical character recognition alone cannot reliably answer the question that fraud analysts care about most: should the lender trust this document?

Lenders need document verification work that combines data extraction with fraud detection. A bank statement may contain readable balances and transaction lines, but the applicant may have edited deposits, removed NSF fees, created the PDF from a fake template, or generated the document with digital tools. A driver’s license may include a plausible name, expiration date, and machine readable zone, but the person presenting the ID document may not match the rightful owner. Biometric verification techniques, such as facial recognition and liveness detection, are increasingly utilized in document verification processes to confirm that the individual presenting the document is the rightful owner.

Document verification methods rely on a combination of visual, physical, and digital checks to prevent fraud and establish identity. Traditional document verification involves a human expert examining documents for tactile features, watermarks, and holograms. Online document verification adds automated scanning, database cross-matching, metadata analysis, security features inspection, and, for identity document verification, facial biometrics. Modern biometric passports and some state ID cards contain microscopic RFID chips that hold cryptographically signed data to verify identity, which adds another validation layer for supported document types.

Document verification is essential for businesses operating in regulated industries such as banking and fintech, as it helps prevent fraud and ensures compliance with regulations like KYC (Know Your Customer) and AML (Anti-Money Laundering). Document verification is also essential for compliance with regulatory frameworks such as KYC, AML, and GDPR, as failure to comply can lead to significant penalties and reputational damage. Regulatory compliance in document verification requires businesses to implement robust verification procedures that satisfy the recommendations of organizations like FATF (Financial Action Task Force) to prevent financial crime.

Inscribe AI addresses this lending-specific need as a category-defining document fraud detection platform built specifically for lenders. Inscribe combines agentic AI with layered fraud detection to automate and enhance manual review processes, helping fraud teams verify document authenticity while preserving explainability for compliance teams.

Manual Review vs Automated Document Verification

Manual verification still plays a role in lending, especially for high-risk cases, unusual documents, complex commercial applications, or escalations that require judgment. But manual document verification is often slow and resource-intensive, requiring human experts to inspect documents for signs of forgery or tampering, which can lead to human error. A trained analyst may spend 30+ minutes on one document set, and complex applications with multiple documents can take much longer.

Manual review also struggles with the fraud patterns lenders now face. Analysts can notice obvious font mismatches, inconsistent logos, or suspicious transaction behavior, but they cannot consistently inspect PDF metadata, detect subtle copy-move artifacts, compare documents against large fraud networks, or identify AI-generated patterns at scale. Reviewer fatigue and subjective interpretation create inconsistent outcomes across teams, shifts, and geographies.

Automated document verification utilizes AI and machine learning technologies to quickly analyze and validate documents, significantly reducing the time required for verification compared to manual processes. Automated document verification can reduce the verification time from days to minutes, enhancing the customer experience by speeding up processes like onboarding and transaction approvals. In some online verification workflows, automated document verification can significantly speed up the customer onboarding process, allowing businesses to onboard new clients in under a minute instead of days with manual reviews.

For lending operations, that speed affects conversion as much as risk. Implementing online document verification can enhance customer experience by reducing onboarding time, which leads to higher conversion rates and improved customer satisfaction. The use of AI and machine learning in document verification helps streamline the onboarding process by quickly validating documents and reducing the risk of human error.

Automated verification also scales differently from human review. While manual verification may be necessary for high-risk cases, automated verification offers scalability and consistency, making it suitable for industries that require large-scale compliance checks. Growing lenders can increase application volume, expand document types, and improve operational efficiency without increasing headcount at the same rate.

Inscribe’s AI Risk Agents perform autonomous forensic analysis of document structure, formatting, metadata, and cross-document context. Instead of forcing compliance officers to interpret a black-box score, Inscribe delivers audit-ready, plain-language explanations that help teams understand why the system flagged a document and whether it needs further review.

Fraud Detection vs Data Extraction

Traditional OCR and IDP tools focus primarily on reading documents. They identify fields such as name, address, employer, salary, transaction amount, account number, expiration date, and tax year. That extracted data helps automate workflows, but it does not prove that the document came from a legitimate source or that the applicant did not manipulate the content.

Fraud detection systems analyze more than the visible text. They examine document structure, formatting, file metadata, visual inconsistencies, template similarities, transaction logic, contextual signals, and cross-document relationships. A fraud detection system may verify document claims against government databases, credit bureaus, Secretary of State filings, web presence, adverse media, employer databases, and other trusted databases.

This distinction becomes critical when lenders review multiple documents from the same applicant. A pay stub may show income that does not appear in bank statements. A utility bill may support proof of address, but the address may conflict with the driver’s license, business license, or tax documents. A business applicant may submit financial records that tell one story while incorporation documents and public filings tell another.

Agentic AI improves this verification process by assigning autonomous fraud analysis tasks across multiple layers. One agent can inspect metadata, another can evaluate visual patterns, another can validate extracted data against external sources, and another can reason across multiple documents. Inscribe uniquely combines deepfake document detection, network analysis, perceptual analysis, and contextual intelligence to catch AI-generated and sophisticated fraud attempts missed by legacy systems.

Automated document verification solutions help businesses maintain compliance by ensuring that all documents are authentic and accurately processed, thus reducing the risk of human error and legal penalties. In lending, the strongest document verification services do both jobs at once: they extract what the underwriter needs and assess whether the document deserves trust.

Types of Financial Documents Verified

Different types of document verification require different fraud signals, validation methods, and escalation logic. Lenders rarely evaluate a single file in isolation; they compare bank statements, income documentation, identity documents, tax documents, business financials, utility bills, legal documents, and other supporting records to form a complete risk picture.

The document verification process typically involves several steps, including document collection, data extraction, validation of authenticity, and manual review if necessary, to ensure that the documents are genuine and have not been tampered with. Inscribe supports this process across document categories by combining automated verification, extracted data, and layered fraud detection.

Bank Statements and Transaction Records

Bank statements and transaction records often carry the highest fraud exposure because they influence cashflow analysis, affordability, credit decisions, merchant cash advance approvals, and small business underwriting. Common manipulation patterns include inflated balances, inserted deposits, deleted overdrafts, fake bank letterheads, altered account numbers, missing pages, changed date ranges, and synthetic transaction histories.

A strong bank statement verification process reviews more than totals. It checks transaction categorization, running balances, recurring deposits, cashflow patterns, account continuity, formatting consistency, and document validation against known bank templates. It also detects whether the applicant created the statement from a blank template instead of downloading an authentic original.

Inscribe’s platform extracts key fields automatically and applies cross-document intelligence to detect inconsistencies and suspicious patterns. For example, Inscribe can compare deposits shown in bank statements against pay stubs, tax documents, invoices, or business revenue claims. That makes bank statement analysis more useful for underwriting and makes fake bank statement detection more reliable for fraud teams.

For lenders that use external banking data, automated systems can cross-reference bank statement claims with available account data, public records, and historical submissions. Even when direct banking access does not exist, AI can assess whether transaction behavior, formatting, metadata, and document structure match expected patterns.

Income Documentation

Income documentation includes pay stubs, W-2s, 1099s, business tax forms, tax returns, and employment verification letters. Fraudsters manipulate these documents to inflate income, fabricate employment, hide instability, or support identity fraud. Common signals include inconsistent pay periods, payroll numbers that do not align, employer addresses that do not exist, mismatched tax IDs, unusual deductions, or income that never appears in bank deposits.

Automated document verification solutions help lenders validate income by extracting wages, employer names, tax identifiers, pay dates, gross and net income, and year-to-date amounts. OCR can read those values, but AI-powered income verification must also test whether the numbers make sense across multiple documents and whether the employer appears legitimate.

Inscribe enriches document data with live research and employer verification to strengthen income verification accuracy. That can include Secretary of State records, adverse media screening, web presence checks, business registration data, employment records, and other trusted databases. When a borrower submits a pay stub from a company that has no credible public footprint, the system can raise a risk signal before underwriting relies on the income claim.

Income documents also benefit from cross-document reasoning. If a W-2 shows one employer, a pay stub shows another, and bank statements show no payroll deposits from either entity, the issue may not appear in a single-document OCR output. Inscribe’s AI Agents evaluate the wider application context so fraud analysts can focus on the highest-risk discrepancies.

Business Financial Documents for Commercial Lending

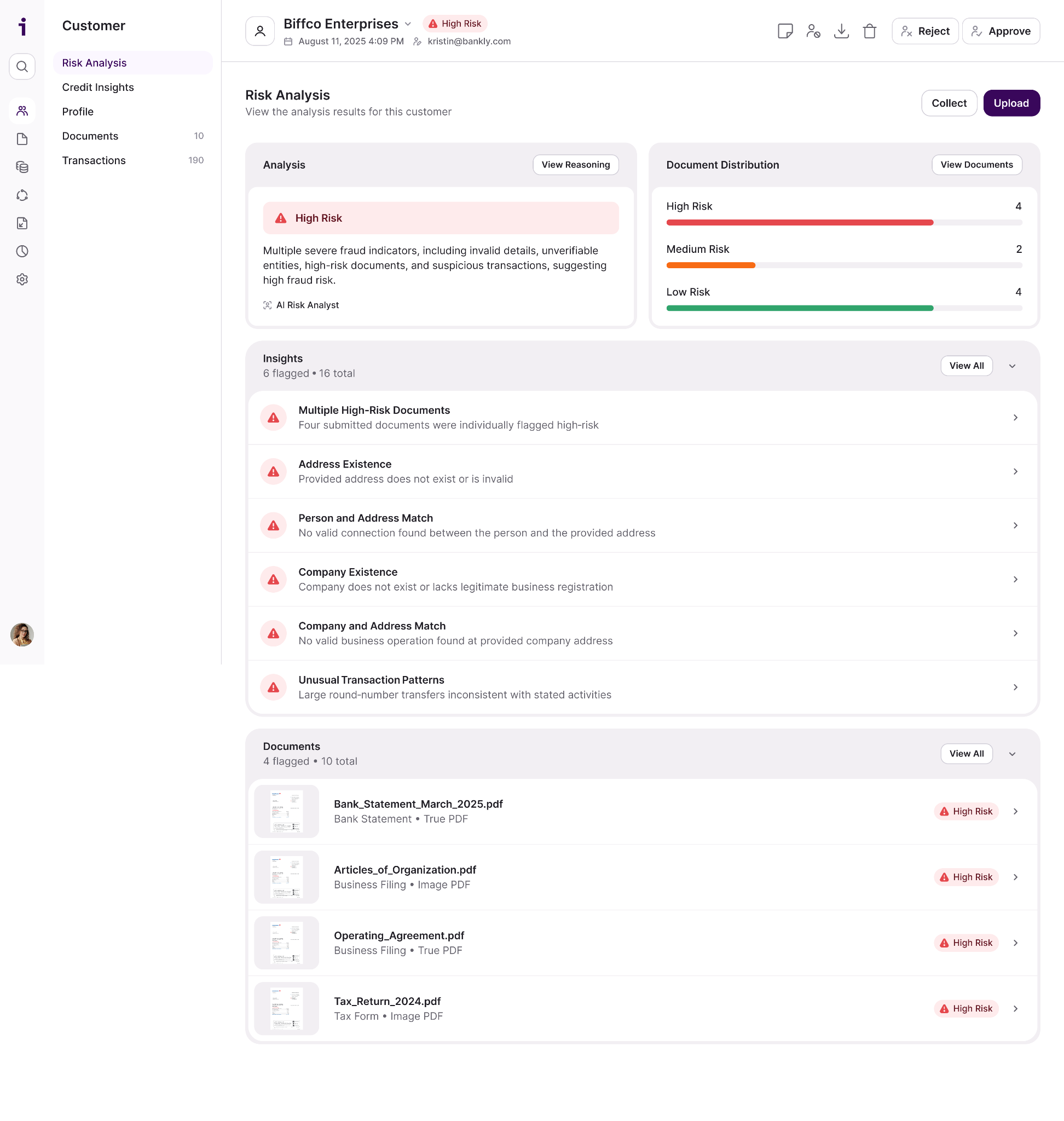

Commercial lending and small business underwriting require broader document validation than consumer lending. Teams may review profit and loss statements, balance sheets, business bank statements, invoices, merchant statements, tax documents, incorporation documents, business licenses, ownership records, and other KYB materials.

Fraud patterns in business documents often involve exaggerated revenue, hidden liabilities, fake invoices, invalid licenses, manipulated ownership structures, and inconsistent business narratives. A business may appear profitable in a P&L while bank statements show declining cashflow. A beneficial owner may appear in one legal document but disappear from another. A company may claim operations in a state where no active registration exists.

KYB document verification requires lenders to verify business existence, status, ownership, licensing, revenue consistency, and legitimacy. Inscribe’s AI Agents synthesize patterns across business documents to identify hidden risks and verify legitimacy. They can compare financial records with public filings, business registrations, address data, and other contextual signals.

This matters for regulatory requirements as well as credit risk. Lenders must assess risk around beneficial ownership, suspicious documents, and financial crime exposure. Strong KYB document verification helps compliance teams ensure regulatory compliance while giving underwriters cleaner evidence for decisioning.

Identity Document Verification and Supporting Documents

Identity and supporting documents include a driver’s license, passport, residence permits, state IDs, utility bills, proof of address documents, and other government issued IDs. These documents support identity verification, id verification, address confirmation, and customer identities across the onboarding process.

Identity document verification focuses on whether the ID document is authentic and whether the person presenting it matches the rightful owner. The most secure document verification systems rely on a multi-layered approach, combining automated scanning with facial biometrics, so lenders can instantly confirm identity or eligibility when the document and biometric signals align. Automated document verification solutions can significantly reduce the risk of fraud by applying multiple layers of checks, such as hologram analysis, liveness detection, and database cross-matching, which can lower financial losses and reputational risk for businesses.

For ID document verification, systems may inspect the machine readable zone, expiration date, document number, fonts, security features, holograms, barcode data, and chip-backed identity information where available. Facial recognition and liveness detection help confirm that the applicant is present and not using a stolen ID, static image, deepfake, or replayed video.

Supporting documents such as utility bills help with proof of address and address verification. But fraud teams still need to validate whether the bill looks authentic, whether the address matches other documents, and whether the applicant’s profile aligns across all collected data.

Inscribe integrates ID document verification with financial document fraud detection, providing a comprehensive view of customer identities and fraud signals. This broader view helps lenders distinguish legitimate users from applicants using stolen documents, synthetic identities, or inconsistent supporting records.

How AI Document Verification Works for Lenders

Modern fraud detection requires layered analysis beyond simple OCR and template matching. Fraudsters now use generative AI, leaked templates, PDF editors, synthetic identity kits, and digital tools that can produce plausible documents at low cost. A rules-only system that checks whether a logo exists or whether a field appears in the right place cannot keep up with that threat model.

Inscribe’s approach starts with document collection from user uploads, then applies automated document verification across data extraction, document authenticity analysis, cross-document reasoning, and escalation. The result gives underwriting, fraud operations, and compliance teams a faster way to verify document claims and decide which cases need further review.

Multi-Layered Fraud Detection Process

A multi-layered verification process reduces dependence on any single signal. A forged document may pass a visual template check but fail metadata analysis. A synthetic pay stub may look clean but fail employer validation. A bank statement may match a known format but reveal impossible transaction sequencing.

For lenders, a practical AI document verification process includes:

- Document collection and quality checks

The system receives physical or digital copies through an upload portal, API, or document collection workflow. It checks blur, glare, cropping, file corruption, and other issues that could affect document validation. - Data extraction with OCR and machine learning

Optical character recognition extracts names, dates, amounts, addresses, account numbers, employer details, tax fields, and other structured values. Machine learning models normalize the extracted data so downstream workflows can use it. - Perceptual and visual analysis

Perceptual analysis examines pixel-level signals, image noise, compression patterns, pasted regions, inconsistent shadows, font differences, and AI-generated artifacts. This helps detect edits that a human reviewer may miss. - Metadata and file structure inspection

AI Risk Agents inspect PDF metadata, creation tools, timestamps, file layers, editing traces, and inconsistencies between document content and file history. Metadata can reveal whether an applicant altered or generated a document. - Network and template analysis

Network analysis identifies recycled templates, suspicious layouts, repeated fraud patterns, and documents connected to known fraud clusters. This helps expose template fraud across multiple submissions and applicants. - Contextual validation and enrichment

Contextual analysis compares multiple documents, validates information against public records, checks employer or business legitimacy, and evaluates whether the application story holds together. - Decisioning, reason codes, and escalation

The system returns risk signals, explanations, and recommended actions. High-confidence clean documents can proceed; suspicious or unsupported cases can route to manual review.

Inscribe’s agentic AI platform continuously adapts to emerging fraud tactics, outperforming static rules-based systems. It delivers results in under 90 seconds for automated review workflows, helping lenders prevent fraud without slowing customer onboarding.

AI Agent Capabilities vs Traditional Rules-Based Systems

Traditional rules-based systems evaluate fixed conditions: expected fonts, known logos, standard field positions, basic checksum rules, visible security features, and predefined document templates. Those checks help with simple fraud, but they often fail when fraudsters use new templates, AI-generated documents, or subtle file manipulation.

AI Agents can reason across multiple layers and update as fraud patterns change. They do not only ask, “Does this document match a rule?” They ask, “Does this document behave like an authentic document, and does it make sense in the context of the full application?”

Inscribe’s AI Agents provide transparent risk signals with forensic detail, enabling faster, more confident decision-making. This matters for compliance officers who need to explain why a lender rejected, escalated, or approved a document. It also helps fraud analysts prioritize cases instead of reviewing every document with the same level of intensity.

Benchmarks across the market show why lenders move from manual processes to AI-powered document verification. ClearStaq reported AI platforms detecting fraudulent bank statements at roughly 94% accuracy versus about 67% for manual review in the MCA sector. Ocrolus has reported 99.2% extraction accuracy for financial documents and improvement in fraud detection from about 45% under manual review to about 89% with AI. These figures illustrate the broader shift: automated systems can review more documents, more consistently, with stronger evidence.

Integration Methods and Workflow Options

Document verification must fit into existing underwriting and fraud operations workflows. Lenders do not need another disconnected review queue; they need verification results where decisions already happen.

Inscribe offers flexible integration options tailored to fintechs, banks, and lenders, ensuring seamless embedding into existing fraud and underwriting workflows. Common implementation paths include:

- API integration for automated underwriting workflows

An API-first approach lets lenders verify document uploads programmatically inside a loan origination system, onboarding flow, or fraud platform. - Document collection portal for customer self-service submission

A document collection experience allows applicants to upload bank statements, pay stubs, tax documents, utility bills, identity documents, and business records with fewer handoffs. - Web application for manual reviews and fraud investigation

Fraud analysts can review flagged documents, risk signals, extracted data, and forensic evidence in one place. - Webhook notifications for real-time decisioning

Webhooks can trigger underwriting actions, fraud holds, requests for additional documentation, or approvals when verification results become available. - Dashboards and reporting for operations teams

Leaders can track fraud rates, manual review volume, false positives, turnaround time, escalation reasons, and operational efficiency.

This integration model supports customer onboarding, ongoing account monitoring, loan renewals, transaction approvals, and KYB reviews. It also helps institutions ensure regulatory compliance by preserving evidence, reason codes, and audit trails for reviewers.

Common Fraud Prevention Signals and Detection Methods

Fraud teams need more than a risk score. They need to understand the fraud signals behind the score so they can calibrate policies, coach reviewers, improve manual review processes, and respond to new fraud tactics. AI-powered document verification should show whether the issue came from file metadata, visual tampering, template reuse, external validation failure, biometric mismatch, or cross-document inconsistency.

Inscribe combines multiple layers of fraud detection to identify fraudulent documents across consumer, SMB, and commercial lending workflows.

AI-Generated Document Detection

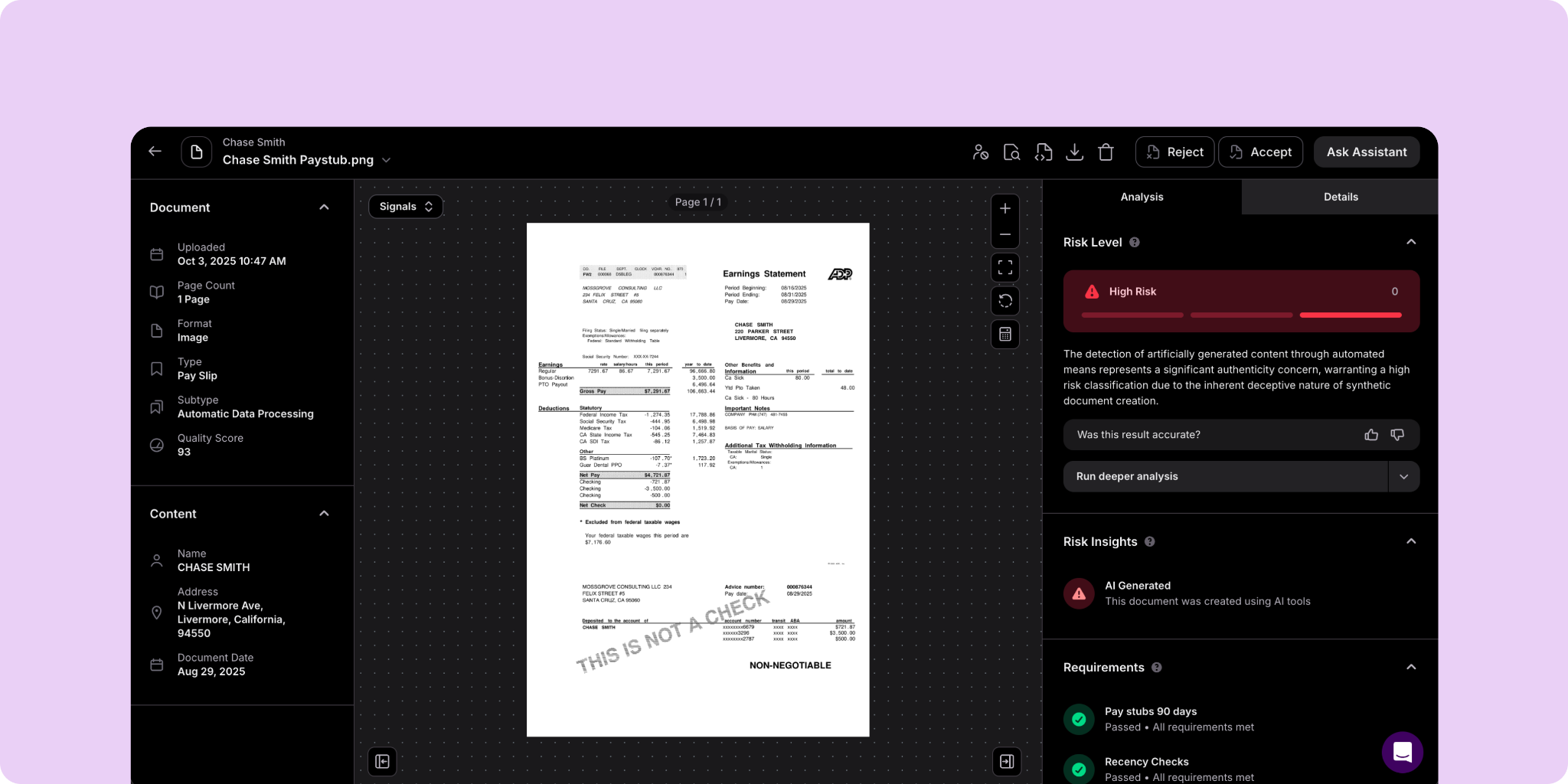

AI-generated document fraud has moved from novelty to operational threat. Fraudsters can now create deepfake financial documents that mimic real bank formatting, produce synthetic pay stubs, fabricate employer letters, and generate entire application packages. These documents may look polished enough to pass manual review.

AI-generated document detection looks for signals that generative systems leave behind. These may include unnatural alignment, overly consistent spacing, repeated visual artifacts, implausible transaction histories, metadata from generative tools, and document structures that do not match how authentic institutions produce files. Pattern recognition can also flag fabricated employment records, synthetic transaction histories, and identity fraud patterns that recur across user uploads.

Inscribe’s proprietary deepfake detection technology identifies AI-generated document artifacts invisible to traditional systems. Its agents inspect file-level signals, perceptual characteristics, formatting, and contextual consistency. If a bank statement looks visually correct but contains generated transaction behavior that conflicts with income documents, the system can surface that discrepancy.

This capability matters because AI-generated fraud does not always look “messy.” Some forged documents look cleaner than authentic scans. Legacy systems that rely on obvious formatting errors often miss these cases.

Traditional Document Manipulation

Traditional manipulation still creates significant risk. Fraudsters use PDF editors, image editing software, and blank templates to alter legitimate documents or create fake ones. Common signals include copy-paste artifacts, font inconsistencies, changed balances, mismatched line spacing, edited dates, inconsistent logos, altered headers, missing pages, suspicious compression, and layout anomalies.

Template fraud creates another challenge. Fraudsters can buy or reuse blank bank statement, pay stub, utility bill, invoice, or tax form templates, then insert applicant-specific data. The document may contain plausible values but lack the file history, structure, and institutional consistency of an authentic original.

Inscribe’s layered detection methods combine perceptual and network analysis to catch these manipulation tactics. Perceptual analysis detects visible and invisible editing artifacts. Network analysis can identify recycled templates, repeated layouts, and patterns that appear across multiple applications. Contextual intelligence then checks whether the manipulated document aligns with other collected data.

Cross-document inconsistencies often reveal coordinated fraud attempts. A manipulated bank statement may support a fake pay stub, but the employer may fail validation. A utility bill may support address confirmation, but the address may not match the customer’s identity profile. A business invoice may support revenue claims, but business bank statements may not show corresponding deposits.

Sophisticated Fraud Schemes

Sophisticated fraud schemes rarely depend on one forged document. They combine identity theft, synthetic identity construction, first-party manipulation, fake employers, shell businesses, and repeated application behavior.

Bust-out fraud may appear across multiple applications when fraudsters build clean-looking profiles, obtain credit, increase exposure, and disappear. Synthetic identity fraud combines legitimate but unconnected document elements, such as a real address, fabricated employment, manipulated bank statements, and a stolen or generated identity document. First-party fraud occurs when customers manipulate their own authentic documents to qualify for credit or better terms.

Inscribe’s cross-document intelligence exposes complex fraud schemes by correlating data across multiple submissions and public records. The platform can identify when the same template, employer, address, account pattern, or document structure appears in suspicious contexts. It can also compare customer identities, financial records, business documents, and trusted databases to identify narratives that do not hold together.

This approach helps lenders assess risk before approval rather than after losses occur. It also reduces customer frustration for legitimate users because the system can separate high-risk patterns from harmless document variation more effectively than blunt rules.

Integration into Lending, Regulatory Compliance, and Risk Management Workflows

Document verification has become essential infrastructure for modern lending operations. It sits at the intersection of underwriting, fraud prevention, identity verification, income verification, KYB, customer onboarding experience, and regulatory compliance. When lenders treat document verification as a downstream manual task, fraud can enter the workflow before risk teams have enough evidence to stop it.

Inscribe’s platform accelerates document fraud detection workflows, reduces manual review by up to 90%, and integrates easily with loan origination and fraud management systems. For teams evaluating automated document verification solutions, the best implementation path starts with operational clarity rather than tool selection alone.

A practical rollout should include:

- Assess current manual review costs and bottlenecks

Measure document volume, review time, fraud losses, false positive rates, manual review backlog, customer drop-off, and escalation reasons. This gives the team a baseline for operational efficiency and fraud prevention. - Identify document types and highest-risk workflows

Prioritize bank statements, pay stubs, tax documents, identity documents, utility bills, invoices, and business documents that most often influence approval decisions or create losses. - Pilot automated verification in a controlled workflow

Start with a defined product, channel, or document type. Compare AI risk signals with existing manual review outcomes, confirmed fraud cases, and customer experience metrics. - Define escalation and policy logic

Decide which results can proceed automatically, which need further review, and which require additional document collection. Human reviewers should focus on ambiguous, unsupported, or high-risk cases. - Integrate with underwriting and fraud systems

Use API connections, webhooks, dashboards, and analyst workspaces to feed verification results into loan origination systems, fraud tools, case management, and compliance reporting. - Monitor performance continuously

Track fraud prevented, false positives, false negatives, processing time, customer satisfaction, review queue volume, cost per document, and losses avoided.

This workflow supports scalability as lending volumes grow and as the institution adds more document types. It also supports related workflow enhancements such as automated underwriting, real-time risk scoring, adverse media review, KYB verification, and compliance audit preparation.

Strong document verification also improves governance. Compliance teams can use reason codes and audit-ready explanations to show that the institution implemented robust controls to prevent fraud, money laundering, and identity fraud. Risk teams can tune thresholds based on product type, geography, applicant segment, or exposure size. Fraud operations teams can update playbooks when Inscribe surfaces new patterns across document submissions.

Frequently Asked Questions

Lenders can verify a wide range of financial, identity, business, and supporting documents. Common examples include bank statements, transaction records, pay stubs, W-2s, 1099s, tax returns, business tax forms, profit and loss statements, balance sheets, invoices, business bank statements, incorporation documents, business licenses, ownership records, driver’s licenses, passports, residence permits, utility bills, and other proof of address documents. Inscribe supports a broad range of document types including driver’s licenses, passports, utility bills, tax forms, invoices, and business incorporation documents. It also supports document verification across major US banks, credit unions, and international financial institutions, with the ability to handle standard formats and non-standard document layouts. The strongest document verification process does not treat every file the same way. Bank statements require transaction analysis and template validation. Pay stubs require employer verification and income consistency checks. Tax documents require field-level extraction and authenticity review. Identity documents require id document verification, security features inspection, and, where appropriate, biometric checks.

AI verification improves speed, consistency, and fraud detection coverage compared with manual review. Manual reviewers often catch obvious fraud, but they face time pressure, human error, fatigue, subjective judgment, and limited ability to detect metadata manipulation, deepfake documents, network-level fraud, or subtle perceptual artifacts. Inscribe’s AI Agents deliver industry-leading precision and speed, significantly reducing operational costs and fraud losses. Automated verification can return results in around 90 seconds or less, while manual verification often takes 30+ minutes per document set and can stretch to days in high-volume queues. Accuracy depends on document type, image quality, geography, and fraud pattern, but industry benchmarks show the direction clearly. AI platforms have reported around 94% detection accuracy for fraudulent bank statements compared with about 67% for manual review in some lending contexts. Other document intelligence benchmarks report extraction accuracy near 99% for financial documents. Well-tuned automated systems also reduce reviewer fatigue and apply the same criteria consistently across applications. False positives still matter. A lender should not optimize only for catching fraud; it should also protect legitimate users from unnecessary customer frustration. The best automated document verification solutions combine high-precision fraud signals with intelligent routing to manual review for uncertain cases.

Document verification typically integrates through API-first architecture, webhooks, document collection portals, web applications, and data exports. Lenders can place online document verification inside customer onboarding, underwriting, fraud review, KYB, account creation, renewal, or transaction approval workflows. Inscribe provides flexible API, web app, and document collection portal options designed for seamless integration into lender workflows. API integrations can connect verification results to loan origination systems, core banking platforms, fraud management systems, and compliance tools. Webhooks can support real-time decision workflows by notifying downstream systems when a document passes, fails, or needs further review. Analyst-facing web applications help fraud teams inspect risk signals, extracted data, and forensic evidence. Dashboards help operations leaders monitor manual review volume, fraud rates, processing times, false positives, and customer onboarding experience. Data exports support audit preparation, model monitoring, and compliance reporting. This integration model lets lenders use automated document verification without removing human judgment where it matters. AI handles high-confidence review at scale; analysts focus on escalations, complex cases, and policy decisions.

Unsupported document types, low-quality uploads, rare international formats, damaged files, or unusual layouts should not force a binary accept-or-reject decision. A mature document verification process routes uncertain cases to manual review, requests resubmission when image quality creates risk, or performs partial verification when full automation is not possible. Inscribe’s platform includes intelligent fallback to manual review and rapid onboarding of new document types to maintain verification coverage and accuracy. If the system cannot confidently verify document authenticity, it can still extract available data, explain the limitation, and send the case for further review with reason codes. This approach helps lenders balance fraud prevention and customer satisfaction. Legitimate users with unusual documents should not fail automatically, while suspicious documents should not pass simply because they fall outside a static rules library. Intelligent fallback gives fraud analysts the context they need to make a defensible decision and helps the platform expand coverage as new document formats appear.

About the author

Brianna Valleskey is the Head of Marketing at Inscribe, where she has spent nearly five years building the company's go-to-market engine from the ground up. She leads demand generation, SEO and AEO strategy, events, content, and marketing operations — and sits at the center of Inscribe's pipeline strategy, working closely with Sales, CS, and EPD to drive growth. She co-hosts the Good Question podcast and produces Inscribe's annual State of Document Fraud report.

Learn More

Dive deeper into document processing

What will our AI Agents find in your documents?

Start your free trial to catch more fraud, faster.